Welcome to Insider Trades Daily, glad you're here! Every day, more than 500,000 investors use this newsletter to track insider buying and selling across major public companies. It’s a simple way to see what the people closest to the business are doing with their own money. Before we start sending your daily updates, there’s just one quick thing left to do. Please confirm your subscription using the link below. Click Here to Confirm Your Subscription to Insider Trades Daily It takes a few seconds and helps make sure your newsletter shows up where it belongs, your inbox, not a spam folder. Once you’re confirmed, we’ll take it from there and deliver clear, no-nonsense insider trading insights straight to you. Start Receiving Insider Information The InsiderTrades.com Team P.S. If there's anything we can do to improve your experience, please let us know by replying to this email.

More Reading from MarketBeat

3 Under-The-Radar Small Caps Making New All-Time HighsAuthor: Dan Schmidt. Originally Published: 5/10/2026.

Key Points

- Small caps often offer the promise of more upside, but also greater volatility and potential for missteps.

- When performing due diligence on small caps, it's important to consider fundamental and technical factors.

- Three small-cap companies—AXT, NWPX Infrastructure, and Arteris—have each surged to new all-time highs, raising questions about the extent of further upside versus profit-taking.

- Special Report: The Biggest IPO Ever: Claim Your Stake Today

When stocks hit all-time highs, investors must decide whether to let winners run or trim positions and take profits. The right move usually depends on your risk tolerance and investment timeline, but it’s important to evaluate each company individually before making buy or sell decisions. In the case of small-cap stocks, you should also be prepared for a fair amount of volatility if you decide to hold. Small caps are more volatile than larger stocks because these companies often have fluctuating revenue and little or even negative net income. Most small caps trade on potential, so risk management is crucial when sizing positions and executing trades. While all-time highs often lead to even higher highs, smaller companies can also experience sharp pullbacks that may offer better entry points if the long-term trend remains intact.

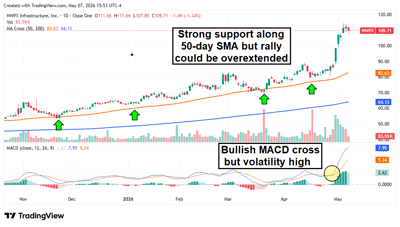

Three small-cap companies recently surged to new all-time highs: AXT Inc. (NASDAQ: AXTI), NWPX Infrastructure (NASDAQ: NWPX), and Arteris Inc. (NASDAQ: AIP). Is it time to take profits, or do these stocks still have more upside ahead? AXT Inc: Feeding the Growing Data Center Power SurgeBased in Fremont, AXT is a semiconductor wafer manufacturer specializing in critical substrates, including indium phosphide (InP). Substrates such as InP are used to connect the photodetectors in high-speed optical transceivers, a vital part of AI data center infrastructure. Data center energy usage is expected to be a major tailwind for companies like AXT; the Lawrence Berkeley National Laboratory estimates that total data center power use could reach 580 TWh by 2028, more than triple what data centers consumed in 2024. InP is the catalyst driving AXTI shares up nearly 600% year-to-date (YTD). During the company’s Q1 2026 earnings call on April 30, management reported $26.9 million in revenue, with InP sales accounting for more than half at $13.6 million. Net losses also narrowed to negative 0.01 cents per share, and the company now projects Q2 EPS between 0.06 cents and 0.08 cents. Both earnings per share (EPS) and revenue exceeded analyst consensus estimates, and the Q2 guide suggests the company is on track for its first profitable quarter since 2022. In addition, a $100 million backlog provides plenty of revenue runway in the years ahead.

AXTI’s 500% surge boosted the company’s market cap to over $7 billion, but the stock now trades at 80 times sales. Investors would be wise to watch for a pullback following April’s $550 million equity raise. Shares stalled around the latest intraday all-time high of $110, allowing the Relative Strength Index (RSI) to move out of overbought territory. However, the Moving Average Convergence Divergence (MACD) indicator formed a bearish crossover, suggesting a slowdown in buying momentum. The long-term growth story remains intact, supported by a strong backlog and data center tailwinds, but valuation and technical signals are short-term red flags. NWPX Infrastructure: Water Infrastructure Supplier With Multi-Decade TailwindsWe now step outside the tech sector for a company with tailwinds that could extend far beyond the AI and data center boom. According to the Environmental Protection Agency (EPA), U.S. water infrastructure will need more than $625 billion in upgrades over the next two decades. Replacing billions of dollars' worth of piping infrastructure is a long-term tailwind for NWPX Infrastructure, which produces pipes and concrete infrastructure. Business is booming so far this year: the company just reported record quarterly revenue of $138 million and EPS of $1.08, with the latter beating consensus by nearly 40%. The company’s backlog now exceeds $430 million, and its cash position is expected to end 2026 within a range of $50 million to $56 million.

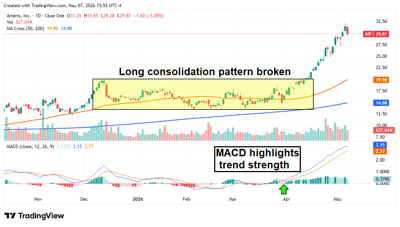

NWPX is up 75% YTD, but it still looks undervalued relative to market averages. The stock trades at just 22 times forward earnings and carries a price-to-sales (P/S) ratio of 2.01, while its balance sheet shows practically no debt. Shares jumped more than 25% in the week following the Q1 2026 earnings beat on April 30, and technical signals suggest the rally could extend further. The stock is now trading well above its 50-day moving average, but there is less concern about a violent pullback given its fundamental strength and relatively low beta (1.06). Arteris Inc: High-Margin Licensing Model Boosted by AI Training WorkloadsArteris is a $1.37 billion market cap “picks and shovels” play in the semiconductor industry. Instead of building fabs to produce chips, Arteris develops interconnect and integration software that connects various CPUs and GPUs. This System-on-a-Chip (SoC) is sold through a typical software model, with high-margin intellectual property licenses that must be renewed. Gross margins reached 92% in fiscal Q4 2025, and the full-year revenue of $70.6 million was a 22% year-over-year increase. The company has long-term structural tailwinds from the growing workload of training AI models, as each GPU cluster requires an IP license to move data.

The stock broke out of a multi-month consolidation pattern following the company’s collaboration announcement with MIPS, gaining more than 60% in just 30 days. The next catalyst is also around the corner; fiscal Q1 2026 results are due May 12, and the company will need to keep posting strong bookings numbers to justify its new valuation. |

0 Response to "Ready when you are"

Post a Comment