You are a free subscriber to Me and the Money Printer. To upgrade to paid and receive the daily Capital Wave Report - which features our Red-Green market signals, subscribe here. I’ll Be Live Here in 15 Minutes

Good morning: Right now, markets are ignoring geopolitical risk and rebuilding carry trades. FX volatility remains near six-year lows despite renewed US-Iran tensions, encouraging investors to borrow in low-yielding currencies such as the franc and yen and buy higher-yielding currencies. The danger sits in Japan, where pension funds may be pushed toward domestic assets, potentially strengthening the yen and disrupting global carry trades. That has basically been the risk all year… and will for a while… All the while, here we go again, with the AI trade stabilizing after a violent momentum unwind. Semiconductors, memory, storage and optical-networking names bounced from their 50-day moving averages as fears of an AI-capex slowdown faded. Reports suggest Meta may double its compute capacity next year, while Micron lifted planned US investment above $250 billion through 2035. Meanwhile, the whole thing centers around inflation… banks are expecting flat to mildly small increases in the June core CPI numbers, with weaker shelter costs and less action on travel. The big wildcards remain memory and electricity costs that are expected to add a lot more to the core PCE outlook. Good thing they’re changing the math on PCE in September… right? Right now, our focus turns to earnings… as analysts expect higher second-quarter numbers with strong revisions to the energy and tech space. We’re seeing a boost to earnings growth expectations for financials, industrials, consumer discretionary and commodities. Good thing we keep printing all this money… TRADERS FOCUS The S&P and the Russell are flat this morning, while the Nasdaq pulls back a little. The tech and hardware names are doing what they have done all week. They run one session, give it back the next. This morning they are handing a bit back again. Oil has come in as well. Brent is back near 76.65, with this week’s war premium draining even as the fighting continues. Under the surface, financials and healthcare are still out front, and small-cap breadth is holding up.

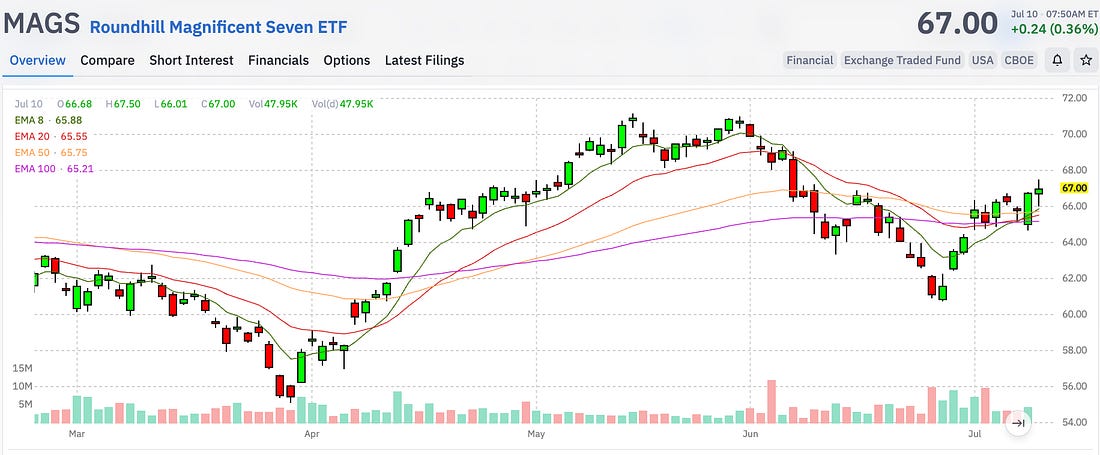

The center of gravity is still the chips, and today they get a new name. SK Hynix comes public with the biggest US listing ever by a foreign company. An IPO that size has to pull its capital from somewhere, and the most likely source is the stocks already tied to the same trade. The Street is drawing the comparison to the SpaceX add. There is already a frenzy around it. Half a dozen leveraged ETFs are launching this week just to trade the thing. That capital pull is the risk for the whole chip group right now. Meta is the one name pushing the other way this morning. It is joining our screamers list on its new paid AI model, Muse Spark, plus its plan to start building chips in-house and rent out its spare compute. A breakout here could finally drag the Roundhill Magnificent Seven ETF (MAGS) through the levels we have been stuck under. It needs to clear 67 and change, with 68.50 the next step.

A move like that would also help the beaten-down communications group off the mat. Delta (DAL) kicked off earnings season this morning, and the quarter was good. It topped its June guidance on about $17.7 billion in revenue and raised its dividend 15%. The stock popped 2% off that, then rolled right over. This is the sell-the-news move, live. Delta has already handed back yesterday’s gain and sits down near 88, holding a little support around 87.50. Watch 87. A break below it is the signal to short the airlines through the JETS. The JETS is already moving, so look for a push toward 31.

There is not a lot on the breakdown list this morning. Not much is being dumped. The one name on it worth watching is Generac (GNRC). It has slipped under its 100-day, but this is mostly profit-taking after the run it was on. Let the MACD build a base and start to curl back. Then you can start selling spreads lower. We like Generac. It is part of that group with Caterpillar and Cummins that can get power online fast, and right now everyone is scrambling for power. Albemarle (ALB) is the other one on that side. This becomes a great buy when the dollar finally starts to cool off. When that happens, you play it the same way, sell a spread lower or just buy the stock and tuck it away. A couple of tech names are back on the breakout side this morning. Datadog (DDOG) looks like it wants to run, but it needs to reclaim its high at 278.71 first. Get above there, and it could find another leg higher. Robinhood (HOOD) has had a huge run since May and is nearing overbought. If you want in, wait for a pullback under the 20-day, then sell spreads under 100. Our triples list is pretty thin right now. The one name on it still building cheap momentum is Baxter (BAX), a $22 stock. Baxter is a big hospital-supply name. They make the everyday stuff, IV bags and infusion pumps. The chart has been stair-stepping lower since 2022 and just getting annihilated. It is finally trying to get up off the floor. It just reclaimed its old breakdown near 22. Stay above it, and healthcare could carry this into a real comeback.

Buy it here and set a stop under the 20-day around 21.35. The next level of support or resistance is 27.50, so you risk a little to make about 20%. Baxter is one of our higher-rated setups this morning. State Street (STT) is also on the list, riding fresh analyst optimism and upgraded estimates, with bullish option flow at 3.1 times its normal volume. State Street reports next week, though, so be careful there. The launchpad is mostly energy again this morning. The top is Ovintiv (OVV). These energy names are all sitting on a pivot with oil and Hormuz, so a lot rides on where the barrel goes from here.

Ovintiv is a mixed producer, heavy oil out of the Permian but a good gas position through its Montney acreage. That gas side matters right now, because Qatar just throttled its giant Ras Laffan plant back to minimum after this week’s attack, leaving a chunk of global supply offline. US gas itself got knocked back on a bigger-than-expected storage build this week. Still, if you are bullish, Ovintiv could run from 54 back toward 60. Earnings are on the 23rd, so you have about two weeks to work with. We are also watching some of the insurance brokers that got hammered when the war kicked off at the start of the year. Marsh McLennan (MRSH), Willis Towers Watson (WTW), and Brown & Brown (BRO) are all finally digging out. The alternative-asset managers are climbing out of the same hole, names like Ares (ARES) and KKR (KKR). For now this is about marking your levels and figuring out where you are comfortable getting back into these names when the time comes. We have options expiring today, so on a Friday let the VWAP be your guide. Delta already made its move, so watch it for the read on the rest of the airlines, and trade the JETS off of it. I will be live in a few minutes to go through what matters most. I hope you can join me. Market outlook

Momentum -- Bounce Back Thursday the market bought back most of the week’s damage in a single session. Stocks ripped across the board, all three of our readings closed green, and the small caps led by a mile. The chips took the headline, with the semiconductor ETF up more than 5%, but the megacaps barely moved the needle. The real horsepower came from the small caps and the beaten-down cyclicals. The one thing to point to was oil. It pulled back from its Iran spike, which took some pressure off the names crude had been crushing, the small caps, the financials, the rate-sensitive stuff. But that is a thin reason for a move this size. There was no data, no headline that changed the setup. After a week like this one, the most beaten-down corners simply bounced the hardest. And nothing underneath really changed. The Fed is still hawkish, rates are still high, and the Iran conflict got worse on the day, not better. Oil pulling back gave the beaten-up names room to breathe, but nothing turned the week around. This morning the bounce is mostly holding, but the chips are already giving a little back. It was a relief, not a resolution. Insider Buying: CEO of Energy Fuels Buys Shares (Blackouts)

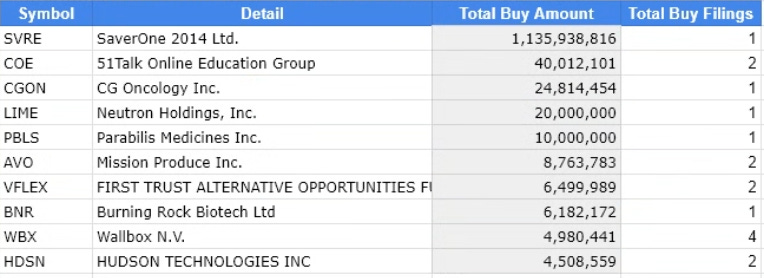

Top Insider Buys of Last 10 Days - Form 4 Documents

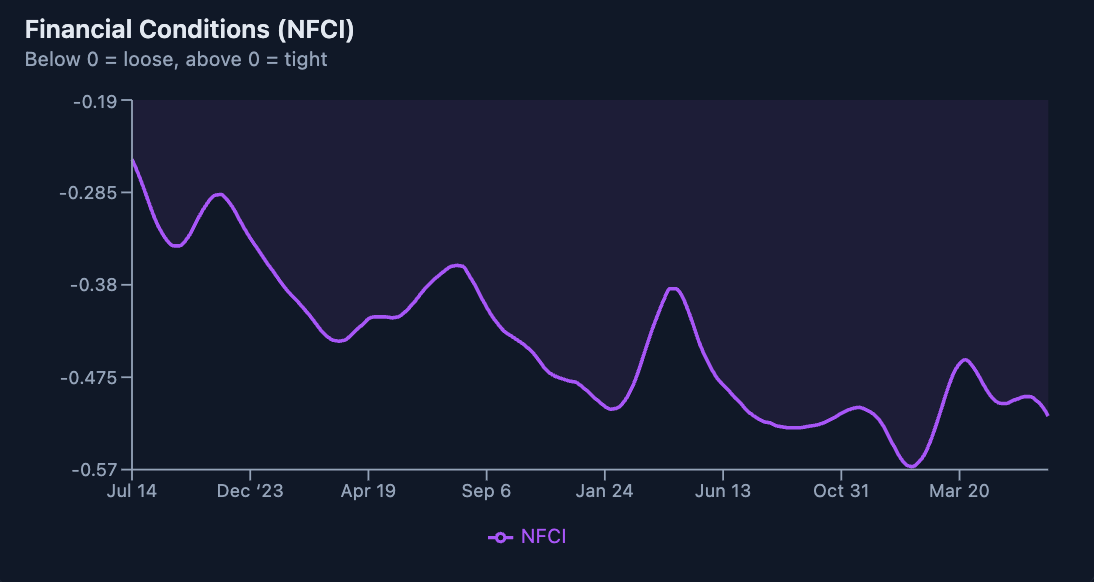

Market Liquidity The Fed spent the week sounding as hawkish as it has in years. Hikes back on the table, higher for longer. But then other people interpretted what was said as cuts are back. And it’s impossible to know how to read any of this without wanting to walk into the woods at times… So… let’s do the obvious, and talk about the balance sheet… Late last year the Fed stopped shrinking that balance sheet and quietly started buying Treasuries again. It has bought bills every month since, and those holdings are growing again. The Fed calls this plumbing, not policy. But money is money, and more of it keeps flowing into the system. By the Chicago Fed’s gauge, financial conditions just eased to their loosest in months, looser now than before the Iran flare-up. That is the balance sheet at work. The Fed is raising the price of money while the quantity keeps climbing, and quantity is what decides whether dips get bought. This week every one of them did, fast.

None of this shows up in a Fed speech, which is why it gets missed. The market is watching the money, not the message, and the money is still loose. The warning will not come from the next hawkish headline. It comes the day the balance sheet turns and conditions start to tighten for real. So far, neither has. Stay positive. Garrett Baldwin About Me and the Money Printer Me and the Money Printer is a daily publication covering the financial markets through three critical equations. We track liquidity (money in the financial system), momentum (where money is moving in the system), and insider buying (where Smart Money at companies is moving their money). Combining these elements with a deep understanding of central banking and how the global system works has allowed us to navigate financial cycles and boost our probability of success as investors and traders. This insight is based on roughly 17 years of intensive academic work at four universities, extensive collaboration with market experts, and the joy of trial and error in research. You can take a free look at our worldview and thesis right here. Disclaimer Nothing in this email should be considered personalized financial advice. While we may answer your general customer questions, we are not licensed under securities laws to guide your investment situation. Do not consider any communication between you and Florida Republic employees as financial advice. The communication in this letter is for information and educational purposes unless otherwise strictly worded as a recommendation. Model portfolios are tracked to showcase a variety of academic, fundamental, and technical tools, and insight is provided to help readers gain knowledge and experience. Readers should not trade if they cannot handle a loss and should not trade more than they can afford to lose. There are large amounts of risk in the equity markets. Consider consulting with a professional before making decisions with your money.

|

||||||||||||||||||||||||||||||||||||||||||||

Subscribe to:

Post Comments (Atom)

0 Response to "What War? What Vol? What Is Happening..."

Post a Comment