| |

|

| Its impact was remarkable. The piece – published on Sunday, February 22 – gave a bleak outlook on the impact of artificial intelligence (AI) on the economy and labor market. |

| The markets responded aggressively. The NASDAQ was down 1.4% the next Monday, and the S&P 500 fell 1.2%. |

| While 100% of the market declines can't be attributed to the fictional thought piece. It was the major contributor, especially for companies named in the post. ServiceNow (NOW), a software company, was identified as being threatened with a theoretical future earnings announcement of a 15% reduction in workforce due to the impact of AI. |

| In real life, ServiceNow collapsed 4.7% on February 23. And there were numerous similar examples. |

| I'm going to share at a high level the thesis of this piece. |

| Contextually, it's timely and good for discussion. But before I go ahead, I have to warn anyone who has anxiety over the impact of AI on work, I don't recommend going further. This is bound to cause convulsions. |

| We should, however, remember that it is only fiction. |

| We're All in Big Trouble, Except for a Few |

| Worth noting is that the primary author of the piece is a former paramedic, med school dropout, who has no experience, training, or education in finance, economics, or technology. |

| The fact that his post was read more than 10 million times and impacted the markets to the extent it did is incredible. But I doubt many at all bothered to understand who was behind this piece of fiction. |

| Citrini's post went along the lines of the following: |

- We'll experience a bull market in 2026.

- In parallel, we'll see waves of layoffs due to "human obsolescence."

- Margins will expand, companies using AI will deliver earnings beats, and stocks will rally.

- Record-level corporate profits will be funneled right back into building more AI infrastructure.

- GDP growth will expand rapidly, but it will be "Ghost GDP" – economic activity by machines will not return to our human economy (i.e., machines don't spend money on goods or services).

- Companies will need fewer workers.

- White-collar layoffs will increase.

- Consumer spending will drop as a result.

- AI agents will remove friction.

- Intermediation, which I have long referred to as friction, will be dismantled.

- Transactions will be automated.

- AI agents won't care about app or brand loyalty.

|

| One of the examples used in the fictional piece was related to the typical 2–3% credit card interchange fees. In the context of machine-to-machine commerce, they make no sense at all. It would be natural for AI agents to look to eliminate those intermediary fees. Blockchain technology and stablecoins provide a perfect solution to do so. |

| In real life, Mastercard (MA) dropped almost 3% the next day, and Visa (V) 2.3% in the two days that followed publishing. |

| The idea was simple: Anywhere where there was friction and complexity, AI agents would be employed to disrupt it. |

| Agents will do the hard work for a fraction of the cost, disrupting those who extracted value by working as an intermediary. |

| But it wasn't all bad. The hypothetical piece did portray winners: |

- NVIDIA (NVDA) continued to post record revenues.

- TSMC (TSM) continued to manufacture semiconductors at 95%+ utilization.

- Hyperscalers were still spending $150–200 billion per quarter on data center construction.

- Taiwan and Korea – because of their exposure to semiconductor manufacturing – outperformed.

|

| But the impact to white-collar workers was particularly bad in this view of the future: |

- White-collar workers would lose their jobs en masse.

- Former high earners would sustain their lifestyle for two or three quarters and then implode.

- Some would adjust and take 50% pay cuts just to stay employed.

- The housing market would suffer badly as many would have to sell their homes.

- Discretionary consumer spending would fall materially.

- Software-centric private equity deals would default on their loans as they were disrupted by AI.

|

| In short, those who had direct exposure to the productivity gains – investors, executives, and owners of computational infrastructure – would be the primary beneficiaries of the AI boom. Those who didn't would suffer. |

| This fictional piece negatively impacted the markets and resonated with so many readers because it played on the fears of what's coming. That, coupled with the reality that many of the future predictions, taken in isolation, are certainly true. |

| I have written about many of these aspects in The Bleeding Edge over the last several years. |

| However, that doesn't make this fictional view of the future entirely accurate. Parts certainly will be, but not the high-level dire predictions about 2028. |

| But perhaps the most ironic part about this fictional thought piece was the clear conflicts of interest. I was surprised at how little attention was given to asking the simple question: Were the authors financially positioned to benefit from what they published? |

| The answer is yes. |

| |

| Follow the Money |

| The founder of Citrini Research is also the principal of Citrinitas Capital Management, an entity that raised $5.05 million from accredited investors a couple of months before publishing the fictional piece. |

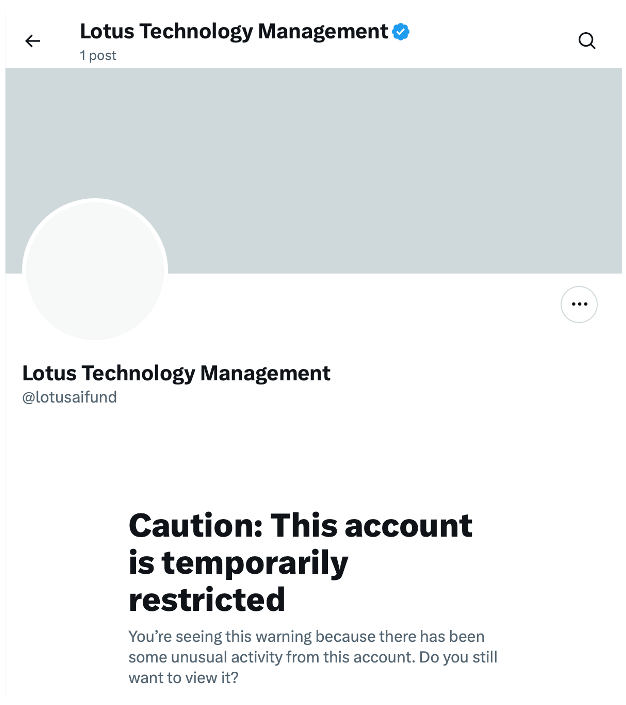

| The co-author of the piece is also a principal of a $262 million, SEC-registered, long/short hedge fund – Lotus Technology Management. |

| Here's where it gets really interesting. |

| Before the market opened on Monday, February 23, the X account for Lotus promoted Citrini Research. |

| That means that the fund was promoting research that it believed would negatively impact certain publicly traded companies, which would then financially benefit the fund's short positions. |

| Shown below, we can see now that the account has been restricted. Never a good sign. |

| |

| And it gets worse, the hedge fund principal at Lotus confirmed on Bloomberg Television after the thought piece was published that his hedge fund already had short positions in companies named in that fictional report. |

| These are the kinds of shenanigans that make me sick about Wall Street. |

| Hedge funds and investment banks quietly build their positions, short or long, into certain companies. They also place their high-net-worth clients into the positions. And then they go public on TV, or on Substack, or on X to flog their thesis to unsuspecting readers/viewers. |

| The goal is to manipulate the markets for their own profits. |

| And clearly, given the market reaction, it worked. |

| More on that in tomorrow's Bleeding Edge… |

| Jeff |

| |

0 Response to "Luddites vs. Effective Acceleration"

Post a Comment