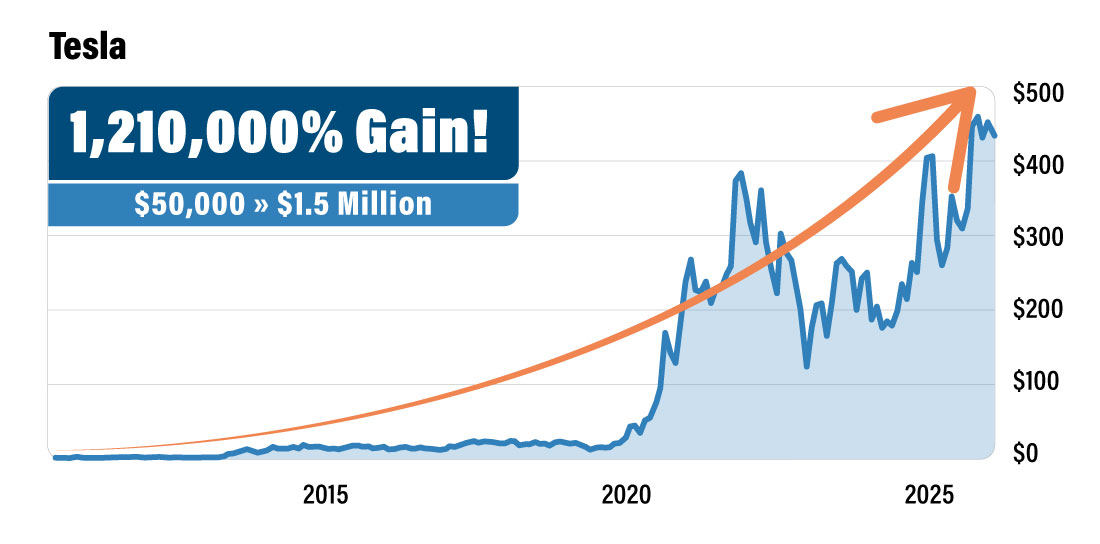

Dear Reader, Dr. Mark Skousen here. Remember Tesla's IPO? It launched at $17 a share…. Most people laughed. Electric cars? That quirky guy who built PayPal? No chance. Of course, not getting in on Tesla was a huge mistake… Today those $17 shares are worth over $250. Early investors who got in pre-IPO and held on could’ve turned a $50,000 investment into $1.5 million over the next decade. How many people do you know who actually bought? Almost nobody, right?!? Well, I was one of the lucky few. I got into a Tesla-heavy fund back when everyone thought Elon's car company would never make a dime. That early bet added nearly seven figures to my net worth over a decade. Now I believe Elon's doing it again. This time with SpaceX. The stakes couldn’t be higher… And I'm betting on him again. Industry experts are calling the SpaceX IPO a "seismic event" — a $1.5 trillion valuation that could be the biggest listing in Wall Street history. Based on my meeting with Elon — combined with my own research — I'm convinced he'll announce the IPO on March 26th. That's less than two weeks from today. If you missed getting in on Tesla pre-IPO... don't make that same mistake twice. And don’t worry. Normally, non-accredited investors are locked out of these types of Pre-IPO opportunities. But… I've found a backdoor that lets you grab a pre-IPO stake before Elon makes the big SpaceX IPO announcement. And I'm sharing the ticker for free. Just click here to see how to get positioned before the big SpaceX announcement. Yours for peace, prosperity, and liberty, AEIOU, Dr. Mark Skousen

Macroeconomic Strategist, The Oxford Club P.S. Bloomberg just reported that S&P is considering a rule change, which could fast-track SpaceX into the index after the IPO. That means billions in forced buying. Get in before that happens. [Click here.]

This Week's Exclusive Content Can Interactive Brokers Repeat Another Big Year?Written by Peter Frank. Posted: 3/19/2026.

Key Points- Interactive Brokers enjoyed strong 2025 growth driven by rising client activity, more accounts, and a technology-driven platform.

- Net income climbed 30% as high margins highlight the firm’s ability to convert revenue into profits.

- Growth depends on active markets and interest rates, so earnings remain sensitive to trading volumes and the macro environment.

- Special Report: 10 Low-Cost Stocks That Could Deliver Outsized Gains

Interactive Brokers Group (NASDAQ: IBKR) had a standout 2025: more customers, more trading, and higher profits. The key question now is whether that momentum can continue. In a highly competitive sector, Interactive Brokers operates as a global online brokerage serving active traders, financial advisors, and institutions. Its strategy rests on two pillars: keeping trading costs low and providing investors with tools typically used by professionals. That technology-focused model helps explain why the company's financial results have been so strong. In 2025, net income available to common shareholders rose 30% to $984 million, while diluted earnings per share climbed 28% to $2.22. Revenue increased 20% to $6.21 billion. Commission revenue jumped 27% to $2.15 billion as trading activity rose, and net interest income grew 13% to $3.56 billion. Because much of the company's infrastructure is automated, a large share of revenue flows to the bottom line. Interactive Brokers reported a pretax profit margin of 77%—up from 71% a year earlier—and that level is impressive for any bank or brokerage. The Continuing Rise of Do-It-Yourself InvestorsThe results reflect a broader, long-term shift in markets: more people managing their own investments through online platforms. Interactive Brokers is seeing growth across options, futures, and equities. During the fourth quarter, daily average revenue trades increased 30% from the prior year. That momentum carried into this year: the company reported 4.4 million daily average revenue trades in February, a 21% increase year over year. Client assets totaled $820 billion, up 40% from a year earlier. Growth is coming not only from existing clients trading more but also from new accounts. The company reported 4.4 million customer accounts at year-end, up 32% from a year earlier; that figure rose to 4.6 million by February. A Growth Play, Not a Yield StockThe company does pay a dividend, but income is not the primary draw for most investors. After a four-for-one stock split in June 2025, Interactive Brokers pays a quarterly dividend of $0.08 per share. At recent prices in the mid-$60s, that translates to a yield of roughly 0.5%. That's modest; the stock's main attraction is its growth profile rather than its payout. Wall Street analysts generally view the company favorably. Its stock is up about 60% over the past year. It has pulled back from a 52-week high of $79.18 in February, but peers in the sector have seen similar moves (see competitors and alternatives). While the company's overall MarketBeat rating is a Moderate Buy, seven of nine firms rate the stock as a Buy. The average 12‑month price target is above $76, and the highest target sits at $91. The Risk of Trading on TradersEven with strong client and revenue growth, investors should be mindful of several risks. Market activity is a major driver of the company's results. When markets are active and investors trade frequently, Interactive Brokers benefits from higher commissions and greater interest income from customer balances. If markets quiet down and trading volumes fall, commission revenue and interest income would likely decline. Competition is also intense. Major firms such as Charles Schwab (NYSE: SCHW) and Fidelity Investments compete at the higher end for investor accounts, while newer apps like Robinhood Markets (NASDAQ: HOOD) focus on attracting younger users with intuitive design and aggressive pricing. Interactive Brokers' low-cost structure, advanced trading tools, and global market access are advantages, but the firm must continue improving its platform to stay ahead. Interest rates are another important variable. In 2025, net interest income of $3.56 billion accounted for more than half of the company's net revenues. If the Federal Reserve cuts rates, that tailwind could fade and earnings growth may slow. Long-term investors need to decide whether they are comfortable with those risks. Interactive Brokers is not a slow, high-dividend financial stock built for stability; it's a fast-growing brokerage that benefits from active markets and rising trading volumes. Still, with strong gains in profits, customer accounts, and assets, Interactive Brokers appears well-positioned for continued expansion. The stock could be volatile if interest rates change or trading activity wanes, but the company remains one of the clearest ways for investors to tap into the global growth of online investing.

This ad is sent on behalf of The Oxford Club. 105 W Monument St, Baltimore, Maryland 21201. If you would like to optout from receiving offers from The Oxford Club please click here |

0 Response to "Remember Tesla?"

Post a Comment