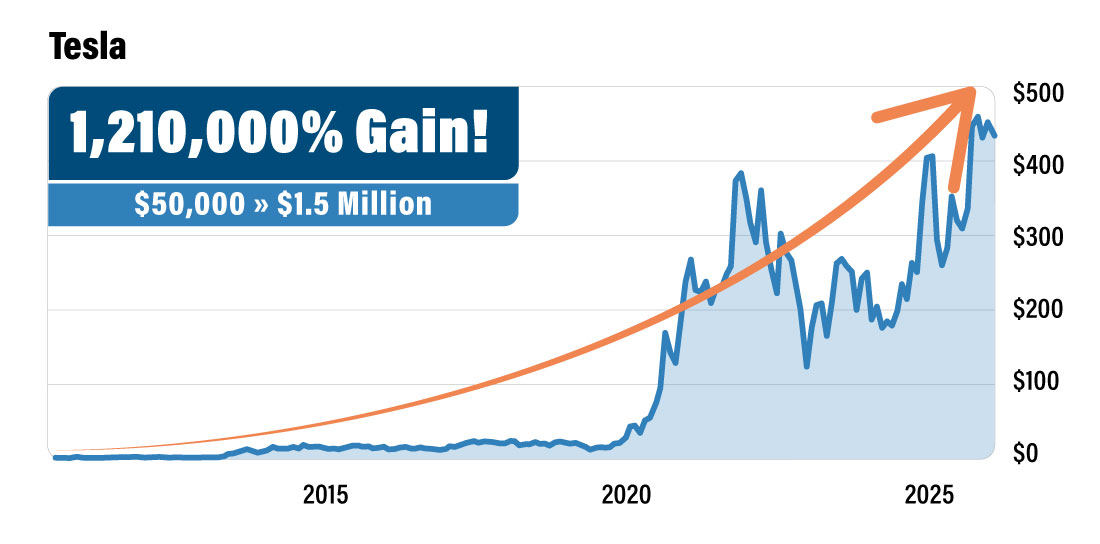

Dear Reader, Dr. Mark Skousen here. Remember Tesla's IPO? It launched at $17 a share…. Most people laughed. Electric cars? That quirky guy who built PayPal? No chance. Of course, not getting in on Tesla was a huge mistake… Today those $17 shares are worth over $250. Early investors who got in pre-IPO and held on could’ve turned a $50,000 investment into $1.5 million over the next decade. How many people do you know who actually bought? Almost nobody, right?!? Well, I was one of the lucky few. I got into a Tesla-heavy fund back when everyone thought Elon's car company would never make a dime. That early bet added nearly seven figures to my net worth over a decade. Now I believe Elon's doing it again. This time with SpaceX. The stakes couldn’t be higher… And I'm betting on him again. Industry experts are calling the SpaceX IPO a "seismic event" — a $1.5 trillion valuation that could be the biggest listing in Wall Street history. Based on my meeting with Elon — combined with my own research — I'm convinced he'll announce the IPO on March 26th. That's less than two weeks from today. If you missed getting in on Tesla pre-IPO... don't make that same mistake twice. And don’t worry. Normally, non-accredited investors are locked out of these types of Pre-IPO opportunities. But… I've found a backdoor that lets you grab a pre-IPO stake before Elon makes the big SpaceX IPO announcement. And I'm sharing the ticker for free. Just click here to see how to get positioned before the big SpaceX announcement. Yours for peace, prosperity, and liberty, AEIOU, Dr. Mark Skousen

Macroeconomic Strategist, The Oxford Club P.S. Bloomberg just reported that S&P is considering a rule change, which could fast-track SpaceX into the index after the IPO. That means billions in forced buying. Get in before that happens. [Click here.]

Special Report Despite Global Tensions, HSBC's Asia Strategy Is Paying OffReported by Peter Frank. Date Posted: 3/13/2026.

Key Points- HSBC’s strategic pivot toward Asia is driving growth as wealth management and cross-border banking expand across the region.

- Strong profitability, rising dividends, and share buybacks highlight HSBC’s focus on returning capital to shareholders.

- The stock has gained more than 50% over the past year as investors grow more optimistic about HSBC’s Asia-focused strategy.

- Special Report: A model just projected 38% downside for the S&P. Do you have a plan?

Global banks face a challenging backdrop. Yet amid the uncertainty, HSBC Holdings (NYSE: HSBC) is holding steady. Based in London, HSBC is Europe’s biggest bank by assets. But don’t be misled by the headquarters: after several years of repositioning to focus on Asia, that region now produces the bulk of the bank’s business—and the strategy is paying off. Few global banks enjoy the geographic advantages HSBC does. Founded in Hong Kong and Shanghai in the 19th century, the institution built deep relationships across Asian financial markets long before many Western competitors entered the region. Those historical ties underpin HSBC’s current approach. Over the past several years the company exited retail banking in the United States, Canada, France, Russia and a handful of other markets. Today, Asia dominates its business, driven by strong performance in wealth management, corporate banking and cross-border services. Last year, Hong Kong operations contributed $15.9 billion of the bank’s $71 billion in revenue—surpassing the U.K. and ranking second only to corporate banking. That cross-border capability has become increasingly valuable as trade and investment flows between Asia, Europe and North America expand. Multinational companies look for banks with global reach and regional expertise, and HSBC fits that profile. HSBC’s Earnings Strength Drives Capital ReturnsThe broader interest-rate environment has helped, too: the bank’s net interest margin and net interest income both rose last year. Overall, HSBC reported a pre-tax profit of $29.9 billion for the year. That was down from the prior year because of one-off charges but still beat expectations. The result produced a net return on tangible equity of 17.2% in 2025—a strong showing for a global bank—and management expects a similar return over the next two years. Income investors should find HSBC attractive. The bank has historically offered a competitive and rising dividend, placing it among the higher-yielding global banks. Management has also stepped up share repurchases. HSBC completed $6 billion in buybacks in 2025, continuing a pattern of returning surplus capital as profitability improves. Those factors support a price-to-earnings ratio of roughly 14, keeping HSBC broadly in line with peers of similar size. While that multiple is below the broader market average, investor caution about geopolitical risks and China’s economic prospects likely plays a role. Analysts Remain Bullish on HSBC’s StrategyDespite solid profitability and shareholder returns, HSBC’s valuation remains relatively modest. Wall Street analysts are nonetheless generally positive on the outlook. The stock recently dipped but remains up more than 50% over the past year, and analysts currently rate the stock a Moderate Buy, citing its strong Asian franchise, improving earnings and shareholder-friendly capital allocation. If HSBC continues to deliver consistent earnings and maintain its dividend, the current valuation could make the stock appealing to investors seeking global financial exposure at a reasonable price. Analysts also point to HSBC’s expanding wealth-management business across Asia as a long-term growth driver as the region’s affluent population grows. HSBC’s Biggest Strength Could Also Be Its Biggest RiskHSBC’s heavy exposure to Asia is a double-edged sword. While it benefits from the region’s growth, the bank’s performance is closely tied to economic conditions in Hong Kong and mainland China; a prolonged slowdown could hurt loan demand and investment activity. Geopolitical tensions are another risk. Operating across multiple regulatory environments exposes HSBC to potential operational and regulatory complications if political disputes between Western governments and China intensify. Currency fluctuations are also a consideration, since HSBC earns revenue in many currencies while reporting largely in U.S. dollars. For investors who believe the global economic center is shifting toward Asia, or who seek dividend income and attractively priced value exposure to global banking, HSBC merits consideration. Over the past decade, HSBC has reshaped itself around Asia’s economic growth and rising wealth, and that strategic shift is increasingly evident in its results. With strong profitability, a high dividend yield, ongoing buybacks and a modest valuation, HSBC may offer investors a compelling mix of income and stability.

This ad is sent on behalf of The Oxford Club. 105 W Monument St, Baltimore, Maryland 21201. If you would like to optout from receiving offers from The Oxford Club please click here |

0 Response to "Remember Tesla?"

Post a Comment