You are a free subscriber to Me and the Money Printer. To upgrade to paid and receive the daily Capital Wave Report - which features our Red-Green market signals, subscribe here. "The Lightning Lost the Game 6-2"What should we make of private credit right now? Just wait for the New York Times' punchline.

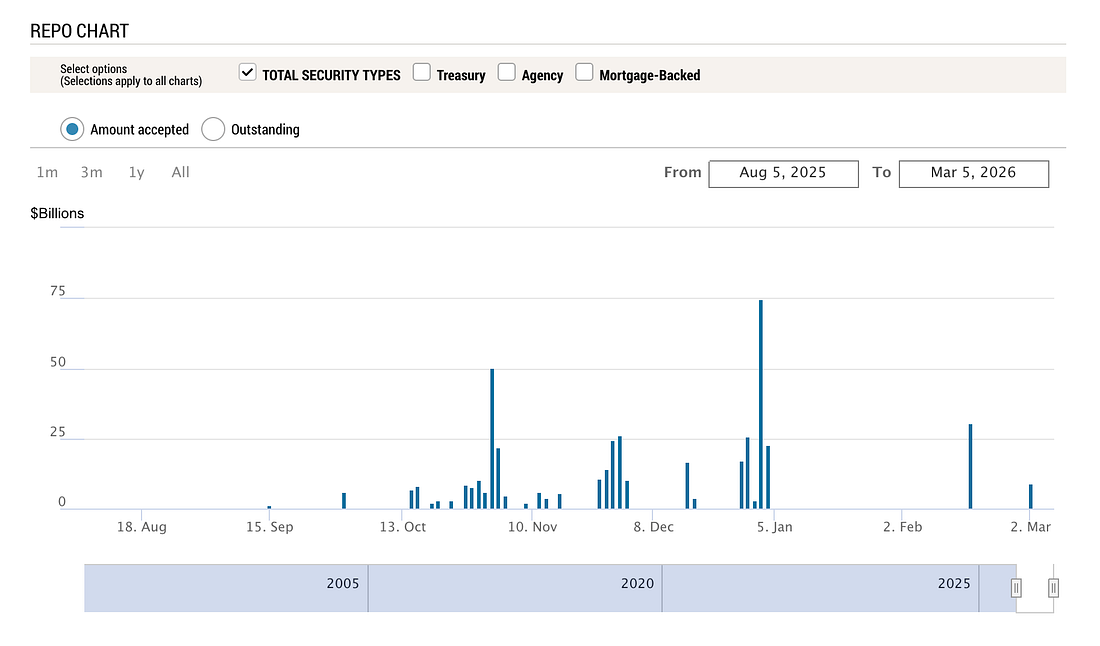

Dear Fellow Traveler: Today, I appeared on The Compound with Michael Batnick and Josh Brown. And if you’re finding yourself here today for the first time… welcome to Me and the Money Printer. Thanks so much for taking the time to visit… During the interview, I was asked, on a scale of 1 to 10, whether I thought private credit was comparable to subprime lending during the 2008 crisis... I said a 7. [Trump voice: Everyone agreed… Hilarity ensued. A good time was had… High fives.] I’m kidding… we had a healthy conversation about the issue… Having spent way too much of my early 30s studying the 2008 crisis… I just want to stress a few similarities… now that I’ve had more time to think about the question. From my side, the current private credit problems are reminiscent of plumbing issues in the shadow banking markets in the past... Not exact. But an issue. As I mentioned last week, the threat of liquidity mismatches is quite apparent. The transparency in this space is poor (you’ll see why soon). And a year ago, Tim Melvin was telling me that the next obvious crisis would come from this world. It’s here, right? But there’s no panic… right? Why? Because we, as a people… well, our moral betters… create “capital” to stabilize this system repeatedly in the post-2008 world and call it something other than QE. We all work for a currency that can be printed… I know that printing isn’t the technical term. It’s called “Reserve creation…” but you get the point. And the markets expect that support... I think that’s been the legacy of the post-2008 Federal Reserve and now Treasury. I argue that if the Fed wasn’t buying roughly $40 billion a month in Treasury bills to stabilize banking reserves, we’d be in a much different and more ominous place. Maybe that’s true in a technical sense. But when central bank balance sheets expand to stabilize collateral markets, the effect on liquidity matters most to investors. Broader “liquidity” has also increased by up to $525 billion, according to CrossBorder Capital and similar estimates. CrossBorder Capital’s measure of global liquidity aggregates central bank balance sheets and cross-border credit flows. The Fed insists these purchases are ‘reserve management,’ not QE. Bond markets know that Treasury Bill purchases are stabilizing… so too are repo operations and reserve injections. I think Jerome Powell and Dallas Fed President Lorie Logan were very transparent about preventing another repo event like the one we saw in 2019. But then Japan and private credit both emerged as additional problems globally. The system commands this constant support… and it receives it. Otherwise, things get really fair, really fast. I somewhat cynically wrote that the deorganizing principle of a government is to print money in February. They keep removing every guardrail, and have done so since Nixon took us off the Gold Standard and/or Lyndon B. Johnson threatened the Fed Chair... They’re not still relying on repo operations because the financial system is robust and healthy.

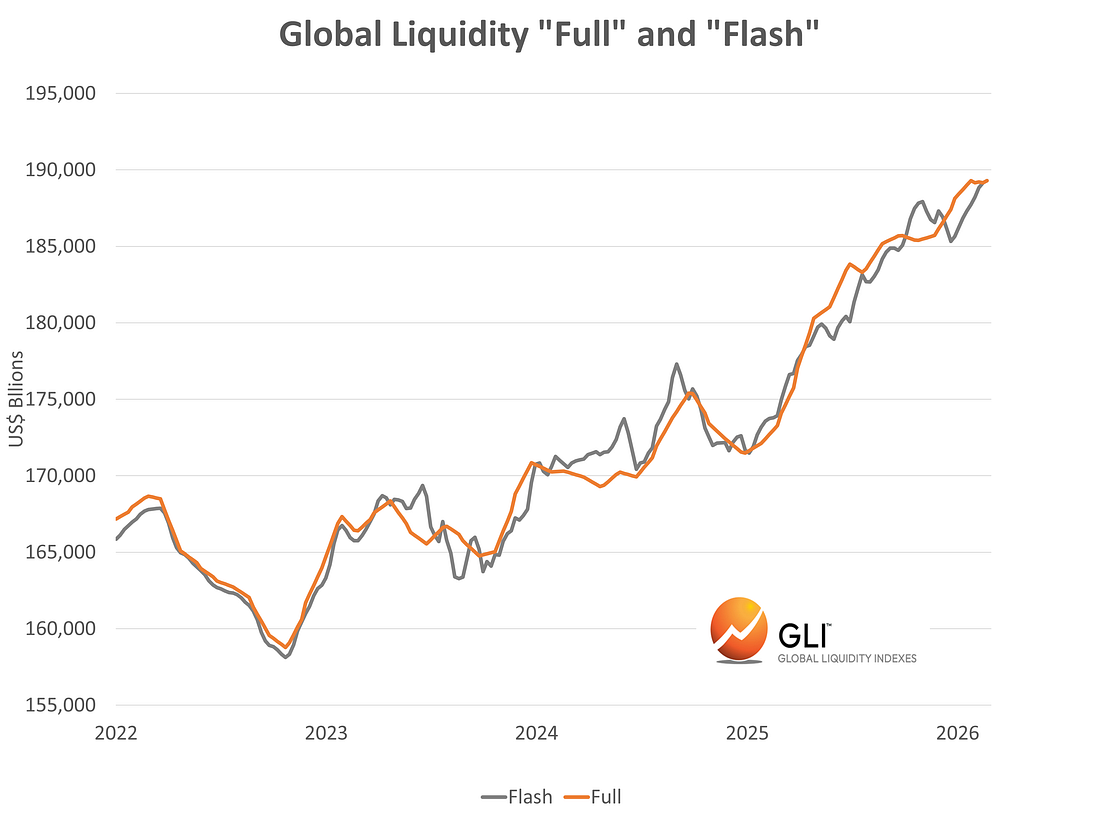

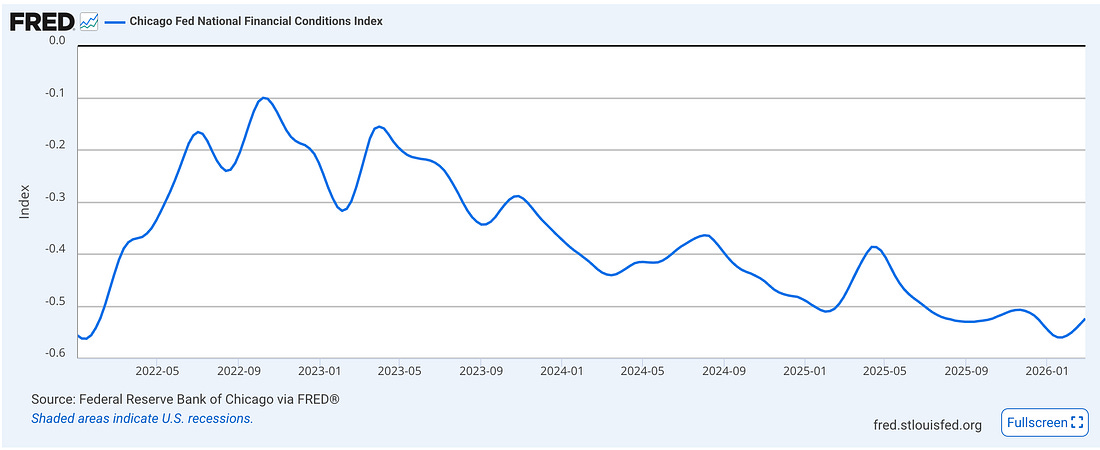

They’re not relaxing bank rules or “welcoming” new classes of Treasury buyers because the system is safe and sound. In March 2023, the Fed created a facility that allowed banks to borrow against underwater bonds at par. Japan has also taken steps to stabilize its bond market and limit forced selling as yields rise. It’s just another day in this crazy system. It’s financial Calvinball… the rules are made up, but they’re never the same as time passes. It’s important to note that something else might “trigger” another bond crisis, liquidity event, or whatever else we want to call it… The war could be one… surging diesel prices are another possibility… sudden risk off-valuation compression events are possible… or maybe it’s something that no one has thought of because it seemed inconsequential at the time. One of the lesser-discussed elements of the 2008 Great Financial Crisis isn’t just that there were origins in the shadow banking system around MBS, but how some analysts believe China’s efforts to curb pollution ahead of the 2008 Summer Olympics may have helped trigger credit problems… long before Lehman collapsed. Trigger is the key term here… Not “caused…” Think of what a trigger is… As in… we’re only one falling snowflake away from causing a temporary avalanche that takes our markets lower… suddenly… like June 2022, March 2023, August 2024, or April 2025... And we're standing on the mountain throwing snowballs at each other for fun… Of course, they could just keep injecting non-QE that aims to achieve QE-like outcomes (stability) or keep issuing more debt at the front of the yield curve (which they will because the system craves it)… but let’s point out the obvious issue. They’ve provided ample support to this financial system between the Fed and the Bank of Japan (and others)… even as we’ve spent time pretending that the Fed Funds rate matters in this discussion, or that we were in some sort of actual tightening cycle between 2022 and 2025 (the Economic Conditions Index suggests otherwise). And fiscal repression will be the norm. What’s more… if this market does burn higher… do we really think at this point that it’s the result of bull or bear spirits… or is it because there is only such thing as a liquid market or an illiquid one… as I contend. This chart from CrossBorder Capital is the biggest open secret in finance… It’s their Global Liquidity Index, which casually tells us a few things we need to know about equity values, market rallies, market downturns, and the relationship between liquidity, momentum, and equity returns at various points in a financial cycle.

It’s not perfect… but it’s a different way of thinking that gives me a lot more confidence and expectations than anything I've learned in graduate school or from trading for 20+ years… The fiscal and monetary base is expanding. It’s clear as day. And that expansion finds itself in risk assets… Run this over the top of the S&P 500 chart back to 2022.

Or layer it on the Economic Conditions Index…

Run this over our momentum indicators dating back to April 2020. It’s very hard to ignore. The ebbs and flows of the market align nicely. It’s just the visual representation of… my crudely described term… BRRRRRRR. It’s not going to last forever. But it just needs to last me one more good run, I hope. Private Credit… A Love StoryI do think the Fed has the guts to create some arcane lending vehicle if they need to… for private credit or anyone for that matter. The precedent is already set by the actions of 2008 and 2020. We keep telling ourselves… well, they’re not going to backstop X, Y, or Z… and then they lend to anyone, everywhere, under some boring financial term no one bothers to look up. If you think that the Fed’s real motivation is Financial Stability (and I do) over say… a dual mandate around jobs and inflation (which feels more like theater these days), it’s not hard to make that prediction and say… Why the hell wouldn’t they create some lending facility for a semi-liquid private credit fund? Is that really far-fetched anymore? I’m not saying it’s going to happen… But let’s be honest with their priorities and mental gymnastics. That said… if private credit isn’t the crisis of our moment, and it can be buttoned up because these assets are illiquid (and maybe that’s possible and the problems pass, but I think unlikely)… there’s one bigger detail that needs to be confronted. I still don’t understand why - after all that’s been revealed in recent months around private credit - we’re still trying to sell retail on private equity vehicles, especially given the fact that we’ve already seen equity tranche positions get smoked… and retail investors are chasing the yield without understanding what they’re actually buying… 15% in yield looks great in a semi-liquid closed-end credit fund… but when you zoom out at a chart of some of these things… it’s just one punch after the next… Wait… never mind. I do understand why they want retail to get into this stuff… It’s Occam’s Razor. Wall Street wants to collect fees. But Benjamin Schiffrin didn’t pull any punches with his headline over at Better Markets.

I don’t see the point in stuffing 401(k)s with this shit… but I’m not incentivized to do so. I’m also the idiot who, back in 2008, thought for a minute that the GFC might change American behavior around speculation, illogical investment strategies, and even the basic concept of greed… similar to what the Depression did to my grandparents. Boy was I wrong… I’d say that we should just let mom-and-pop own Apple and Exxon and not hold the private equity bag in a liquidity or debt crisis… because that, honestly, is likely how we’re going to turn this into an MBS-like event at some point. But I know what would be coming from some public relations shop in Washington, D.C., because I used to work for one. The writers at the advocacy centers in National Harbor or Foggy Bottom would say I’m “anti-capitalist” or that I oppose giving investors the “same rights and financial freedom” as big institutions. And that’s… “Unamerican” to not let mom-and-pop invest in a Cayman-domiciled, quarterly-liquidity, subordinated tranche interval fund backed by leveraged loans to AI startups that haven't generated revenue yet. Damn it! If I were in the business of mud-slinging on behalf of an alternative asset advocacy or lobbying shop, that’s the exact language that would be proposed at critics of these policies to expand private equity assets into retail retirement accounts. And that will be the end of the debate because that’s how that PR works. But I’ll laugh because retail investors rarely get access to the best private deals. They get access to scaled products designed for distribution. That’s how all this works. At some point, someone in Washington is going to suggest we put Bitcoin in school lunch programs during a crypto winter and call it “financial literacy.” What Is Real?I’ve said alot… But I want to highlight two articles on private credit that show how divided we are in our understanding of the gravity of the situation and what separates certain classes of investors at this moment... Matt Levine’s Money Stuff column this week laid out the illiquidity premium with the kind of calm, detached precision that makes him one of my favorite financial writers… His argument is clean... institutional pools of capital like pension funds have predictable cash needs… Therefore, they can afford to lock money up for the long term… They receive a premium for handling that illiquidity. Individual investors can’t do this or won’t do this… they might need capital back tomorrow, so they lean harder into liquid investments. Cool… That means we’re all playing in different sandboxes… with different needs. But, now we’re in a situation where individual investors are panicking and pulling money from funds like Blue Owl’s OBDC II… That makes the illiquidity premium blow out… So, now Boaz Weinstein starts calling around and offering 65 cents on the dollar because he can instantly provide the liquidity a panicking investor now wants... This almost feels like some sort of intellectual puzzle. Here we are with a structure that offers a unique opportunity for those investors with long-term payout horizons, but more importantly, a strong tolerance for volatility... And I get that… and agree that these can be good things… and I want private equity exposure because I understand the J-curve and the upside of good deal flow… But then, all I could picture was Matthew McConaughey doing this in the background…

And I had to go pet my dogs and calm down… It’s a smart way of thinking… but it’s a reminder that this game isn’t for everyone... So, why are we trying to make it one… a game for everyone? Private credit and private equity don’t need more investors. They need better managers and due diligence... The Best End to a Financial Article EverAll this brings me to the New York Times piece by Rob Copeland and Maureen Farrell on private credit and the clown show at Blue Owl… After two paragraphs of this article, you’re in a completely different world. The authors say that Blue Owl is trying to convince investors that its $300 billion portfolio is worth what it claims… The company held two packed calls with financial advisers, urging them to stick with the fund. That was happening too back in 2008… while I’m not precisely comparing the 2008 GFC to what's happening now… there’s a lot of rhyme… Remember the line from Too Big to Fail… where Bart McDade tells Dick Fuld… If this stock keeps falling, “your traders are going to jump ship…” That’s what this reminded me of… They’re losing people's confidence… not just their money. That matters. It’s not just about the redemptions… It’s about the quality of the assets, and we’re still trying to figure out what a lot of this stuff is and what it’s really worth. Blue Owl sold $1.4 billion in loans. Part of that sale went to a closely affiliated insurer that it didn’t initially disclose to investors… That’s the kind of detail that makes me wonder… Why? And then get this… emphasis mine.

I’m sorry… read that last sentence again… And check to make sure that your nose doesn’t start bleeding. That isn’t a Ponzi scheme… It’s not. It's just a liquidity transformation vehicle, with the transformation mechanism being leverage. Depending on your level of cynicism, it’s either a perfectly normal feature of modern finance or just a highly questionable investment vehicle in a very nice tie. The authors write that in a private note to investors, Rubric Capital called Cliffwater “a canary in a coal mine” and suggested it could be “the first domino in the bank run we foresee.” The first opportunity for investors to withdraw capital from the fund is next week, and Rubric is discussing the possibility of bank runs. So… we’re not facing a 2008-like threat. But maybe 2023? Or sort of 2020? With parts of April 2025. Or Archegos-lite? Or… how far back do we need to go here… Or maybe something new that we haven’t considered yet… because virtually no one predicted the Silicon Valley Bank crisis… Seriously… when you consider all this, and you step back… and you’re under 50, you realize that your entire life has just been moving from one financial crisis to the next… and every time people say… “Well, this is different because...” or “This isn’t like 2008…” Have you considered the non-stop stress of it all because this market is anchored by non-stop monetary and fiscal intervention from every central bank and has been this way since the GFC... I have a very long memory… and it’s all in the data… And there’s no accountability for any of it… because “This is just how it is now.” The Bank for International Settlements has warned for years about cross-border monetary spillovers and debt rollover risks… That’s what made their admission about the impact of one central bank’s actions on another economy so haunting… and evidence suggests that we’re just going to live like this for another 25 years with K-shaped recovery after K-shaped recovery, or we’re going to have a real economic crisis in the next decade that can’t keep our surging debt obligations in line. Or both… It’s just a continued feeling of suspended animation… Director and screenwriter Harold Ramis once said he always envisioned that Bill Murray lived the same day in Groundhog Day for a little more than three decades…

Well… I’m halfway there. I’ll leave you with this… It’s the real highlight of the article. It’s almost like the New York Times knows that there isn’t going to be any accountability here, so they drop one of the funniest digs I’ve read in a while… Doug Ostrover, Blue Owl’s co-CEO, took out personal loans last year on the back of then-skyrocketing Blue Owl stock to buy a stake in the Tampa Bay Lightning. He just spent his Saturday buying shots for strangers at a Lightning game while his stock sat 60% below its peak… Seriously… The New York Times article concludes with this… Emphasis mine.

That last line… pointing out that the Lightning lost that game is brutal. The authors, Copeland and Farrell, didn't need to include it. They wanted to. That's the difference between reporting and writing. This is the same week, the same industry, and two completely different emotional registers. And maybe there is enough monetary support right now. Maybe people look at BDCs and think it’s a generational buying opportunity. Or maybe… for ONCE… we find out how big the financial holes are… and we don’t kick the can down the road to the inevitable. But I doubt it. In the end, there’s only one go-to solution… And everyone from Ben Bernanke to Janet Yellen, from the Bank of Japan to the People’s Bank of China, from Steven Mnuchin to Scott Bessent… and everyone else running laps at the Bank for International Settlements… It’s all very clear where we are. It’s a fiat monetary system increasingly dependent on refinancing debt that can only be managed through continual rollover. It’s been that way since at least 1971… or maybe since LBJ broke the stability of the post-War Era, and our debt just keeps spinning higher… faster. And until there is a massive shift in the monetary order, all roads point to more monetary and fiscal expansion in the long term… Which is bullish for equities, right? I see it clearly because it’s all I’ve seen everywhere since 2008. So let’s keep our eye on momentum and liquidity… And just wait around for the next big… BRRRRRRRRRRRRRRRRR. It’s the same story… every day. Live from Punxsutawney… I’m Phil Connors. Stay positive, Garrett Baldwin About Me and the Money Printer Me and the Money Printer is a daily publication covering the financial markets through three critical equations. We track liquidity (money in the financial system), momentum (where money is moving in the system), and insider buying (where Smart Money at companies is moving their money). Combining these elements with a deep understanding of central banking and how the global system works has allowed us to navigate financial cycles and boost our probability of success as investors and traders. This insight is based on roughly 17 years of intensive academic work at four universities, extensive collaboration with market experts, and the joy of trial and error in research. You can take a free look at our worldview and thesis right here. Disclaimer Nothing in this email should be considered personalized financial advice. While we may answer your general customer questions, we are not licensed under securities laws to guide your investment situation. Do not consider any communication between you and Florida Republic employees as financial advice. The communication in this letter is for information and educational purposes unless otherwise strictly worded as a recommendation. Model portfolios are tracked to showcase a variety of academic, fundamental, and technical tools, and insight is provided to help readers gain knowledge and experience. Readers should not trade if they cannot handle a loss and should not trade more than they can afford to lose. There are large amounts of risk in the equity markets. Consider consulting with a professional before making decisions with your money.

|

Subscribe to:

Post Comments (Atom)

0 Response to ""The Lightning Lost the Game 6-2""

Post a Comment