If you're looking for the best place to invest $1,000 right now…

Forget about AI…

Forget about nuclear energy, quantum computing and crypto.

This dwarfs all of it… combined.

Here's the story…

President Trump just signed this bill into law, forcing the immediate replacement of ALL the plumbing under our $382 trillion financial system.

Just like the plumbing under your house moves water, there's plumbing under our economy that moves money. And right now America's "financial plumbing" is 50 years old.

It's slow, it's clunky and it breaks all the time…

However, thanks to a breakthrough new technology that BlackRock CEO Larry Fink is calling "the next major evolution in market infrastructure", there's finally a replacement…

Insiders are calling it The New American Money Grid.

And thanks to this legal mandate that just left President Trump's Desk…

Every financial asset in America MUST be moved onto this New American Money Grid by April 2027.

And once it's in place, every transaction on the New American Money Grid will burn a scarce "Digital Fuel" and that's what this new interview is about.

Getting you in on the ground floor of this little-known asset set to potentially EXPLODE as the trillions starts moving in the coming weeks.

Unfortunately major institutions like BlackRock, Fidelity and Grayscale are already backing up the truck, quietly positioning themselves before the news goes mainstream.

So you don't have long to act.

That's why we brought in legendary tech investor Andy Howard to provide the full details.

UiPath Fell on Good News—That Could Be the Opportunity

Authored by Thomas Hughes. Publication Date: 3/12/2026.

Key Points

- UiPath is on track to accelerate AI adoption, outperforming expectations and raising guidance.

- Analysts and institutional trends reflect accumulation and market support, downside is limited in 2026.

- Capital returns, specifically share buybacks, underpin a robust outlook for a stock rebound.

- Special Report: Elon Musk already made me a "wealthy man"

UiPath (NYSE: PATH) appears poised for a bullish reversal after a March pullback that looks like an overreaction to otherwise positive news. The company's Q4 fiscal year 2026 (FY2026) results topped expectations, with 13.4% revenue growth and net income more than doubling, yet shares retraced.

The more likely outcome is that accelerating adoption of agentic AI—reflected in the company's updated guidance—will drive stronger growth and outperformance in coming quarters, producing bullish cycles and an uptrend in the stock.

How to collect micro-royalties from ChatGPT (Ad)

Take a look at this image of an AI data center—thousands of them are popping up across America, but one popping up in West Texas is much different from all the others. When it's complete, it will be surrounded by armed guards, razor wire, and 24/7 surveillance, with billions of AI prompts running through this building every single day.

What most folks don't know is that you can collect a micro-royalty each time—every ChatGPT query, every Alexa answer, every Netflix recommendation could put money in your pocket. This single opportunity has already paid out over $810 million since 2022, and Marc Lichtenfeld found a way to collect up to 16 income payouts a year from it.

Click here to see Marc's full briefingTechnically, the setup resembles a head-and-shoulders reversal. Because the pattern has a downside bias, the market could trade sideways for a period before completing a full reversal, but current action suggests the bottom may be in.

Key support sits at $10.75, with resistance near $12.25 likely to be tested (and perhaps broken) soon. Over the longer term, a move above $13.50 would be a more convincing bullish signal, taking the stock above the pattern's initial shoulder and setting it up for a sustainable rally.

Market Data Reflects Support and Accumulation of PATH Stock

Analysts' reactions to the earnings were mixed. Some focused on cautious elements of the guidance and trimmed targets, while others upgraded the stock, citing strong net-new annual recurring revenue growth, robust free cash flow, and the company's shift to agentic AI. That shift—from rules-based automation to reasoning, task-performing AI agents—is strategically significant.

Despite the mixed headlines, the underlying data suggest the stock is buyable. The 18 analysts tracked by MarketBeat rate it a Hold, with a consensus price target near $15, implying roughly 30% upside. That level would push the stock back above its 150-day exponential moving average (EMA), a key barometer of longer-term investor sentiment and institutional activity.

Institutional ownership is notable: institutions own more than 60% of the shares, providing meaningful support and showing accumulation into 2026. Activity was especially pronounced in the first quarter of calendar 2026, when total trading spiked and buying accelerated—roughly $3 bought for every $2 sold in the opening two months. Early price action suggests that someone is buying this dip.

Under the Hood: UiPath's Q4 Was Better Than the Stock Suggests

The quarter's strength was broad-based across licenses, subscriptions, and services, driven by new client wins and improved retention. Annual recurring revenue expanded by a net 11%, supported by a 7% lift in retention revenue. Margins showed leverage and quality improvements, and cash flow was strong: free cash flow totaled $182 million (38% of revenue) with essentially 100% conversion.

Free cash flow matters because UiPath is not only profitable but returning capital to shareholders. The company does not pay dividends, but it has actively repurchased shares, reducing the share count by an aggressive 3.8% in FY2026. While buyback activity may moderate in FY2027, management announced a new $500 million repurchase authorization to replace the prior $1 billion program.

UiPath's balance sheet shows no obvious red flags. A small reduction in cash and current assets was offset by increases in total assets, resulting in higher equity and persistently low leverage. Total liabilities remain below equity and only modestly above cash. The company is well positioned to invest to support its strategy. Near-term catalysts include the integration of WorkFusion, continued product innovation, and accelerating adoption of agentic AI.

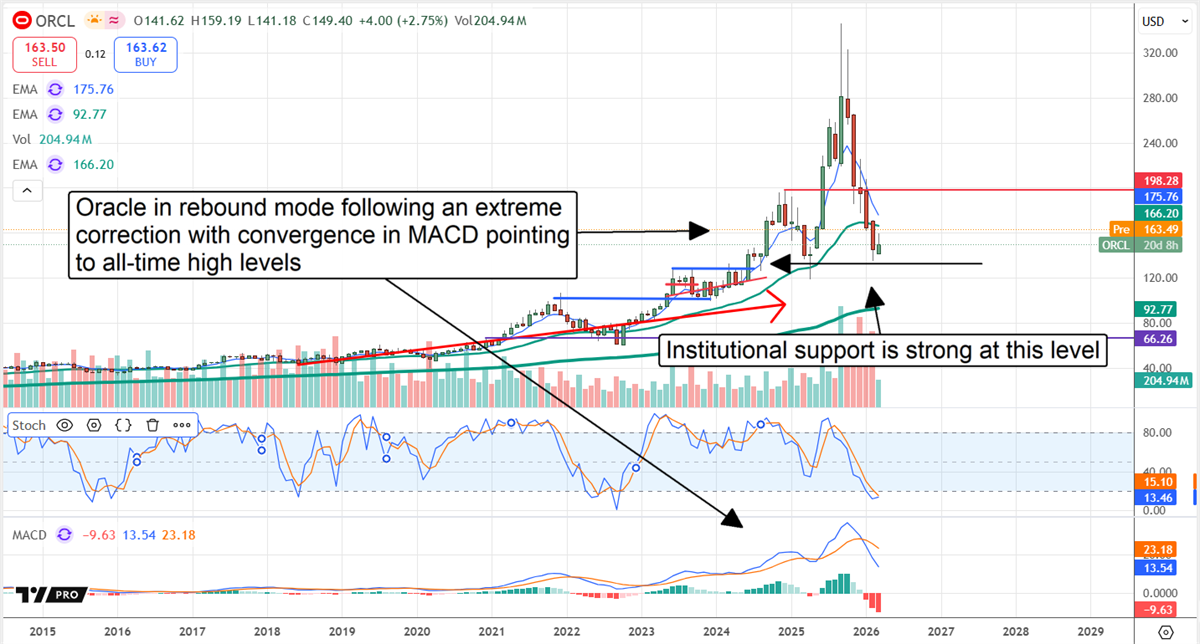

Oracle Speaks! The Message: AI Demand Outpaces Capacity

Authored by Thomas Hughes. Publication Date: 3/11/2026.

Key Points

- Oracle's Q3 release affirms its robust outlook and upped the ante with improved long-term guidance, and the analysts liked it.

- Price target increases and upgrades point to rising share prices and the potential for a robust rebound and fresh all-time highs.

- Institutions accumulated in Q1 when prices were low, providing a support base and limiting risk in 2026.

- Special Report: Elon Musk already made me a "wealthy man"

Oracle's (NYSE: ORCL) stock price could be poised to experience the hottest upswing in modern tech history. The company's fiscal Q3 2026 release not only affirmed the robust outlook and allayed debt-related fears, it also raised forward guidance.

The takeaway for investors is that, in the words of JPMorgan (NYSE: JPM) analysts (who upgraded the stock), the report provides the clearest proof yet that Oracle's AI strategy is working. Oracle is emerging as a powerhouse of AI innovation, supplying the infrastructure to support AI, the tools to develop it, and the applications built on it — all while delivering improving services to both legacy and new clients.

Analysts, Institutional Buying, and Price Action Align: Robust Rebound Brewing

How to collect micro-royalties from ChatGPT (Ad)

Take a look at this image of an AI data center—thousands of them are popping up across America, but one popping up in West Texas is much different from all the others. When it's complete, it will be surrounded by armed guards, razor wire, and 24/7 surveillance, with billions of AI prompts running through this building every single day.

What most folks don't know is that you can collect a micro-royalty each time—every ChatGPT query, every Alexa answer, every Netflix recommendation could put money in your pocket. This single opportunity has already paid out over $810 million since 2022, and Marc Lichtenfeld found a way to collect up to 16 income payouts a year from it.

Click here to see Marc's full briefingAnalysts are responding as expected — either reaffirming already bullish outlooks, issuing upgrades, or raising price targets. Sentiment has shifted back to an aggressively bullish posture, reversing prior price-target reductions, strengthening the Strong Buy rating, and improving the rebound outlook.

As it stands, the bias is firmly bullish: 75% of ratings are Buy or better, the single Sell rating is more than a year old, and the consensus price target implies about an 80% upside from the pre-release close, with trends pointing toward the high end of the range. The high end is pegged at $400 — more than 165% upside — and could be reached well before year-end.

Institutional trends also align with a bottom in price action and an outlook for sustained upward momentum. While institutions sold on balance in Q4 2025, that bearish behavior ended with the turn of the year as they reverted to net accumulation.

Early Q1 activity shows more than $1.50 bought for each $1 sold, providing a tangible tailwind that is likely to strengthen as the year progresses.

And the charts back it up: daily, weekly, and monthly indicators show the market was deeply oversold and is set up for a bullish momentum swing. The likely outcome is a retest of the all-time high, with potential to exceed it by roughly $140 or about 100%. The $140 figure is a base-case derived from the magnitude of Oracle's recent pullback; a break to new highs would signal trend continuation and could produce a move roughly equal to the prior advance in dollar terms or percentage terms — $140 or about 100%.

Oracle Rebounds on Outperformance and Acceleration

Oracle delivered its strongest quarter in more than 15 years in Q3. Revenue rose more than 21% to $17.19 billion, accelerating both sequentially and year over year (YOY), and outpacing consensus by 165 basis points. Strength came across the business, led by a 44% increase in total cloud revenue. Total cloud revenue grew 44% to nearly $9 billion, representing almost 52% of total revenue. Cloud infrastructure revenue surged 84%, supported by a 531% increase in Multi-Cloud Database revenue and a 243% gain in AI infrastructure. SaaS revenue grew 13%, driven by gains in Fusion and NetSuite.

Margin performance was also solid. The company leveraged revenue strength to surpass consensus earnings estimates despite increased spending and higher leverage. Adjusted EPS of $1.70 beat expectations by a wide margin (about 590 basis points), drove significant cash flow, and management expects the strength to continue.

Guidance is likely to propel the stock higher now that the rebound is underway. Oracle issued strong guidance for Q4, implying better-than-expected full-year results, and raised its outlook for the following year. Oracle now expects revenue growth to accelerate to over 31% annually, outpacing estimates for both revenue and earnings by sizable margins. A key driver will be rapid expansion of cloud and AI capacity, with at least another 14 hyperscaler instances — roughly a 25% increase — coming online in the near term.

Oracle's Debt: Not So Much a Concern as a Necessity

Oracle's debt and share count have grown to support its expanding AI network. While concerns about leverage are understandable, they reflect the financing needed to scale quickly. Q3 results and the company's swelling backlog — now $553 million, up 325% YOY — suggest rapid expansion is required or another competitor will capture the opportunity.

The key detail for investors is that the backlog remains more than 4.4 times the company's debt, equivalent to roughly eight years of business at the Q3 pace, and will be recognized much more quickly. That dynamic should enable rapid debt reduction and the buildup of shareholder equity in coming years. Risks include the potential need for additional capital, but those risks will be mitigated if the backlog continues to grow.

to bring you the latest market-moving news.

This email message is a sponsored email sent on behalf of Awesomely, LLC dba TickerReport, a third-party advertiser of TickerReport and MarketBeat.

Contact Us | Unsubscribe

© 2006-2026 MarketBeat Media, LLC dba TickerReport. All rights reserved.

345 North Reid Place #620, Sioux Falls, SD 57103. United States..

0 Response to "Trump's New Money Grid"

Post a Comment