Dear Reader,

Dr. Mark Skousen here.

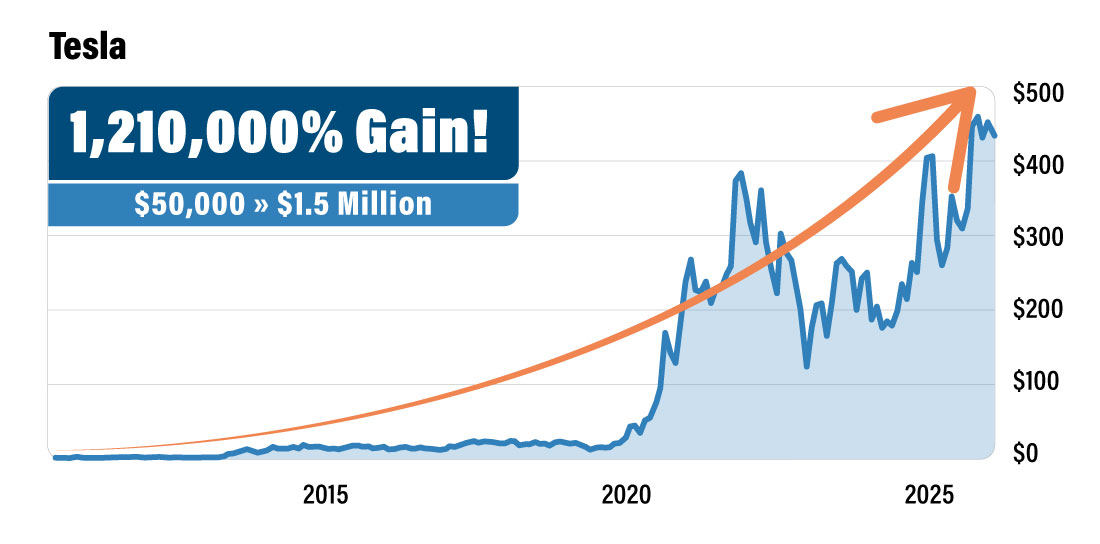

Remember Tesla's IPO?

It launched at $17 a share….

Most people laughed.

Electric cars? That quirky guy who built PayPal?

No chance.

Of course, not getting in on Tesla was a huge mistake…

Today those $17 shares are worth over $250.

Early investors who got in pre-IPO and held on could’ve turned a $50,000 investment into $1.5 million over the next decade.

|

How many people do you know who actually bought?

Almost nobody, right?!?

Well, I was one of the lucky few.

I got into a Tesla-heavy fund back when everyone thought Elon's car company would never make a dime. That early bet added nearly seven figures to my net worth over a decade.

Now I believe Elon's doing it again. This time with SpaceX.

The stakes couldn’t be higher…

And I'm betting on him again.

Industry experts are calling the SpaceX IPO a "seismic event" — a $1.5 trillion valuation that could be the biggest listing in Wall Street history.

Based on my meeting with Elon — combined with my own research — I'm convinced he'll announce the IPO on April 20th.

That's less than two weeks from today.

If you missed getting in on Tesla pre-IPO... don't make that same mistake twice.

And don’t worry. Normally, non-accredited investors are locked out of these types of Pre-IPO opportunities.

But…

I've found a backdoor that lets you grab a pre-IPO stake before Elon makes the big SpaceX IPO announcement.

And I'm sharing the ticker for free.

Just click here to see how to get positioned before the big SpaceX announcement.

Yours for peace, prosperity, and liberty, AEIOU,

Dr. Mark Skousen

Macroeconomic Strategist, The Oxford Club

P.S. Bloomberg just reported that S&P is considering a rule change, which could fast-track SpaceX into the index after the IPO. That means billions in forced buying. Get in before that happens. [Click here.]

Lilly's Next Empire: A $10 Billion Bet on AI and Neuroscience

Submitted by Jeffrey Neal Johnson. Originally Published: 4/2/2026.

In a powerful demonstration of financial strength and strategic foresight, Eli Lilly and Company (NYSE: LLY) recently committed more than $10 billion to two major initiatives in a matter of days. While many market participants remain focused on Eli Lilly's dominance in the diabetes and obesity markets, Lilly is already deploying cash flow from its tirzepatide franchise, which includes Mounjaro and Zepbound, to build its next growth engines.

This capital deployment is a coordinated, two-pronged strategy. Eli Lilly is simultaneously modernizing how it discovers medicines by investing heavily in artificial intelligence (AI) and expanding its product line by moving decisively into the multi-billion-dollar market for sleep-wake disorders. The dual approach signals an evolution in the company's strategy, positioning Eli Lilly to justify its premium valuation and secure leadership for the next decade.

Pillar 1: A Wager on Smarter Science

Eli Lilly's first major move was to significantly expand its partnership with InSilico Medicine, in a deal valued at up to $2.75 billion. This is more than a typical research collaboration; it is a sizable bet on the future of pharmaceutical development and places Lilly at the forefront of an industry trend. Big pharma increasingly turns to AI to address its longest-standing challenge: the slow, costly, and inefficient R&D process.

Major U.S. Gov't Gold Announcement Coming April 15? (Ad)

A former Pentagon and CIA advisor is flagging April 15 as a critical date for gold investors. He says the U.S. government is set to grant final authorization for mining operations at what he believes is the largest gold deposit in the world.

The company behind it trades at just $2 per share and has largely flown under the radar. He believes early investors positioned before the announcement stand to benefit most.

View his full analysis and see the details behind this gold playKey Points

Eli Lilly is pioneering the future of drug development by making a substantial investment in artificial intelligence to accelerate its research process.

The company is strategically expanding into the high-growth neuroscience market with a significant acquisition, securing a promising new revenue stream.

These investments in technology and diversification reinforce Eli Lilly's strategy to secure its long-term industry leadership and growth trajectory.

- Special Report: Have $500? Invest in Elon's AI Masterplan

In traditional pharmaceutical research, identifying a promising drug candidate can take years of painstaking trial and error. AI-powered platforms, like those developed by InSilico, use advanced algorithms to analyze vast amounts of biological data.

That capability enables researchers to identify potential molecules and therapeutic targets with greater speed and precision than is humanly possible. The goal is to dramatically shorten the notoriously long and expensive timeline—often 10 to 15 years and costing billions of dollars—required to bring a new treatment from the laboratory to the pharmacy.

The implications go beyond efficiency. By leveraging AI, Lilly could tackle complex diseases and identify novel drug targets previously considered undruggable, opening new avenues for breakthrough therapies. For investors, this tech-forward strategy is significant: it helps shift the R&D pipeline from a major cost center to a more predictable asset and directly addresses one of the biggest long-term risks for any pharmaceutical company—the patent cliff. By building a more productive R&D process, Eli Lilly is working to ensure a steady stream of new products, supporting a higher, more stable valuation over the long term.

Pillar 2: Buying a New Growth Engine

Almost immediately after announcing its expanded AI partnership, Eli Lilly unveiled its second strategic pillar: the acquisition of Centessa Pharmaceuticals (NASDAQ: CNTA). The deal includes a $6.3 billion upfront cash payment, with the total value potentially reaching $7.8 billion if certain milestones are achieved. This is a classic strategy to secure future growth by acquiring a promising late-stage pipeline in a therapeutic area with significant unmet needs.

The centerpiece of the transaction is Centessa's portfolio of orexin receptor 2 (OX2R) agonists, a novel class of medicines for treating sleep-wake disorders. The lead candidate, cleminorexton, has shown potential to be a best-in-class treatment for conditions such as narcolepsy and idiopathic hypersomnia. Many existing treatments for these debilitating disorders have undesirable side effects or are controlled substances, creating a substantial opportunity for a safer, more effective alternative.

This acquisition propels Eli Lilly into a leading position within the multi-billion-dollar neuroscience segment. It directly addresses a primary investor concern for companies that rely heavily on a blockbuster drug: the need for revenue diversification. While the success of its GLP-1 franchise is a major strength today, this deal helps ensure Lilly's future is not solely dependent on a single class of medicine. For Eli Lilly's stock price, adding a high-potential asset like cleminorexton creates a clear path to a new revenue stream, making future earnings more robust and providing a strong defense against market shifts or increased competition.

Owning a New Kind of Industry Leader

Eli Lilly's recent strategic actions are more than the sum of their parts. The two deals are complementary and form a cohesive vision for the future: the InSilico partnership modernizes drug discovery to make it faster and more efficient, while the Centessa acquisition adds a high-potential product to the pipeline, securing a new source of future revenue. This proactive strategy contrasts with the complacency that has challenged market leaders in other industries and shows a management team that is building for the future while at the peak of its current success.

This forward-looking approach is precisely what is needed to support Eli Lilly's sizeable $836.9 billion market capitalization and its premium price-to-earnings ratio of over 40. A valuation of this magnitude demands a clear narrative of sustained, long-term growth. These investments provide that narrative, demonstrating that management is not resting on its laurels but actively constructing the next iteration of Eli Lilly.

The company is executing a blueprint for a new kind of industry leader: a biotech–tech hybrid that marries best-in-class science with advanced technology. For investors, these actions are strong evidence of a durable, diversified growth platform and reinforce the case for Eli Lilly as a foundational holding in the future of healthcare innovation.

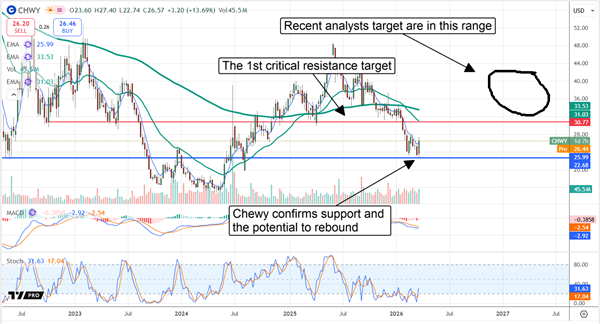

Chewy Gobbles up Market Share in 2026: Poised to Advance in Q2

By Thomas Hughes. Posted: 3/27/2026.

Key Points

- Chewy is on track to rebound in 2026 as its growth, margin, and cash flow invigorate buyers to action.

- Industry-leading growth and market share gains underpin the outlook.

- Optimistic earnings outlook triggered a buying event, confirming support at a critical level.

- Special Report: Have $500? Invest in Elon's AI Masterplan

Chewy (NYSE: CHWY) stock faces headwinds in 2026, as do many retailers. However, its digital-first, asset-light model is gaining share, evidenced by an industry-leading growth pace. Chewy consistently outgrows peers and the broader pet-care industry, helped by rising digital penetration and greater focus on nutrition and pet healthcare. The takeaway for investors is that the stock rallied by double digits after an otherwise tepid release, indicating market support and potential for further gains this year.

Chewy Leads Market in Q4: Guides for Strength in 2026

Chewy delivered a solid quarter despite a tough year-ago comparison and analysts' expectations. The company reported $3.26 billion in net revenue, a 0.5% increase on an as-reported basis and an 8.1% increase on an adjusted basis (the adjustment reflects an extra week). Chewy's performance was driven by a 4% increase in active customers, a 2.2% rise in sales per active user, and a 4.8% gain in autoship sales.

Major U.S. Gov't Gold Announcement Coming April 15? (Ad)

A former Pentagon and CIA advisor is flagging April 15 as a critical date for gold investors. He says the U.S. government is set to grant final authorization for mining operations at what he believes is the largest gold deposit in the world.

The company behind it trades at just $2 per share and has largely flown under the radar. He believes early investors positioned before the announcement stand to benefit most.

View his full analysis and see the details behind this gold playAutoship is a critical part of the business because it represents recurring monthly revenue tied to food, medicine, and healthcare products. Autoship accounts for roughly 84% of net sales, providing Chewy a stable foundation to accelerate growth in 2026 and giving investors clearer revenue visibility.

Margin news was mixed. The company widened margins across the board, which helped drive a 30.4% increase in adjusted EBITDA, a 72% increase in net income, and a 47% increase in free cash flow (FCF). Still, the results were slightly shy of some expectations.

Adjusted earnings per share (EPS) declined by one cent year over year and missed consensus, but the quarter was strong enough to build cash on the balance sheet while maintaining a low-debt profile and continuing share repurchases.

Chewy's buybacks aren't robust and failed to significantly reduce the share count in fiscal 2026, though they largely offset share-based compensation and could be stepped up over time. Management is forecasting margin improvement and an accelerated pace of earnings growth. The long-term outlook calls for a high‑teens to low‑20s % compound annual EPS growth rate, which implies the stock trades at roughly 9x its projected 2031 EPS—suggesting material upside over the coming years.

Guidance drove CHWY's post-release price action. The company's revenue forecast met expectations, and its earnings outlook was bullish: management projects FY2027 adjusted EPS of about $13.68, nearly a dime above MarketBeat's consensus.

Analysts Put Bottom in Chewy Stock: Institutions Pose Risk

The analyst response to the release was mixed: early notes included optimistic commentary on earnings strength and 2026 guidance, offset by several price target reductions. The net result is that Chewy's Moderate Buy rating and 80% Buy-side bias remain intact, although the consensus price target was trimmed. That consensus still implies roughly 60% upside this year, but many of the post-release revisions landed toward the lower end of the prior range.

Even so, the updated targets suggest some upside potential, with most projections in the 20% to 50% range. These targets support Chewy stock's potential to rebound, setting the stage for positive revisions later in the year if execution continues.

Institutional ownership is a key risk. Institutions own more than 90% of Chewy's shares and were net sellers in early Q1. If that selling pressure persists into Q2 2026, CHWY will likely struggle to clear critical resistance near $20.75, a level that may be tested before the quarter ends. Conversely, renewed institutional accumulation would help solidify the market bottom and create potential for a meaningful rebound.

Chewy's catalysts include execution of its high-margin strategies: Chewy Vet Care, private label expansion, AI-driven efficiencies, and its advertising business. The ad business enables manufacturers to target consumers on a pay-per-click basis, while AI supports operational efficiency across the digital ecosystem. Private-label growth not only boosts margins but also helps capture share from premium brands.

This message is a paid sponsorship sent on behalf of The Oxford Club, a third-party advertiser of MarketBeat. Why did I get this email message?.

This ad is sent on behalf of The Oxford Club. 105 W Monument St, Baltimore, Maryland 21201. If you would like to optout from receiving offers from The Oxford Club please click here

If you need assistance with your subscription, please contact our South Dakota based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC. All rights reserved.

345 N Reid Pl., Sixth Floor, Sioux Falls, S.D. 57103-7078. United States of America..

0 Response to "Remember Tesla?"

Post a Comment