You are a free subscriber to Me and the Money Printer. To upgrade to paid and receive the daily Capital Wave Report - which features our Red-Green market signals, subscribe here. Five "WTF Moments" from the BIS Quarterly ReviewMy brain hurts... "why... they... have... make... finance... so hard..." Dear Fellow Traveler: Poll the average American. They’ll be able to tell you the name of the company behind Tostitos and probably every baseball team in the American League East. But can they tell you about the Federal Reserve's dual mandate? Only 6% can… Now… ask them if they can tell you what the Bank for International Settlements does. I’d be shocked if 1 in 300 people knew what it is. Well, long story short, it’s a bunch of economists over in Basel, Switzerland… The BIS is the central bank for central banks, overseeing domestic banks. Think of it when a five-year-old is shown a dusty picture of another woman on a bicycle from the 1930s and told… “This is Mommy’s… Mommy’s… Mommy…” The BIS focuses on “fostering monetary and financial stability by encouraging the cooperation of domestic systems.” Each quarter, they release a report … appropriately (and almost as if forced to) called the Quarterly Review. Each is a giant exercise in seeing how many footnotes an economist can include... I haven’t met anyone else who reads them. If you go to a dinner party and say, “I just finished the BIS Quarterly Review,” people will assume you’re either lying or going through something. The writing is so dry it could be used as a fire retardant. Which is fitting, because the things they write about are usually on fire. Now… when the BIS is worried about something, it means the rest of us should have been worried about it six months ago… (or we were, and people told us we were wrong and told us to go sit down…) The BIS flagged growing fragility in credit markets before 2008. They flagged dollar funding stress before March 2020. They don’t scream, and maybe that’s the problem. The March 2026 edition just dropped. I read every page, including the footnotes, because I’m going through something. Here are five moments where I put the PDF down and stared at the wall. 1. Big Tech Is Borrowing Money You Can’t SeeWe know that Big Tech is taking on massive amounts of debt to build AI data centers. The same centers that spend hundreds of billions on chips and servers and whatever else make a chatbot that tells you the right way to fry an egg over medium (guilty). The BIS says these companies issued over $100 billion in bonds in 2025 alone. That’s a lot of borrowing, but that’s just the part you can see. The part you can’t see is what the BIS describes as “shadow borrowing.” Shadow borrowing? That sounds insane…

These companies are setting up separate legal entities, sort of like shell companies, and borrowing through them using private credit firms. Think of it like putting a mortgage in your cousin’s name so it doesn’t show up on your credit report. The debt still exists… but your financial profile looks clean. If their borrowing is larger than it appears… and the BIS is saying it is… then the risk is larger than it appears, too. I go into the numbers in the video above… Credit default swaps on these companies are already getting more expensive. And JPMorgan is eager to sell new ways to hedge AI debt risk… because of course. 2. $500 Billion in Software Loans Got a Wake-Up Call from AI For the past decade, private credit funds have been lending enormous sums to software companies… the ones that sell subscriptions to businesses. Think cloud storage, project management tools, and payroll software. The loans grew from $8 billion in 2015 to over $500 billion by the end of 2025. That’s about 19% of total direct lending in private credit. That sounds like way too much money to lend to companies that might all have one possible catalyst that might fuel their demise…

Well… AI finally entered the conversation… Suddenly, investors started wondering whether all those software companies would still have customers in five years. Software stocks dropped about 30% in four months. The funds holding these loans saw their stock prices fall around 10%. And the gap between what these funds say their loans are worth and what the market thinks they’re worth kept widening. That gap is called a “discount to net asset value,” and when it’s growing, it means the market is saying: “We think you’re lying about your book.” Some funds have started blocking investors from withdrawing their money. Remember, gates don’t contain a fire. They just trap everyone inside the building while the temperature rises. 3. A Financial Product Crashed Silver 30% in a Single DaySilver had doubled in 2025, then gained another 50% in January 2026 alone. The BIS dug into the fund flow data and found that retail investors were the main source of inflows into silver and gold ETFs during the rally. Institutional investors, meanwhile, held steady or actually trimmed their positions. So the run-up was driven almost entirely by smaller investors piling into leveraged ETFs... products that use borrowed money to amplify gains. A leveraged ETF sounds crazy, right?

If silver rises 2%, a 2x leveraged silver ETF rises 4%. Sounds great on the way up.

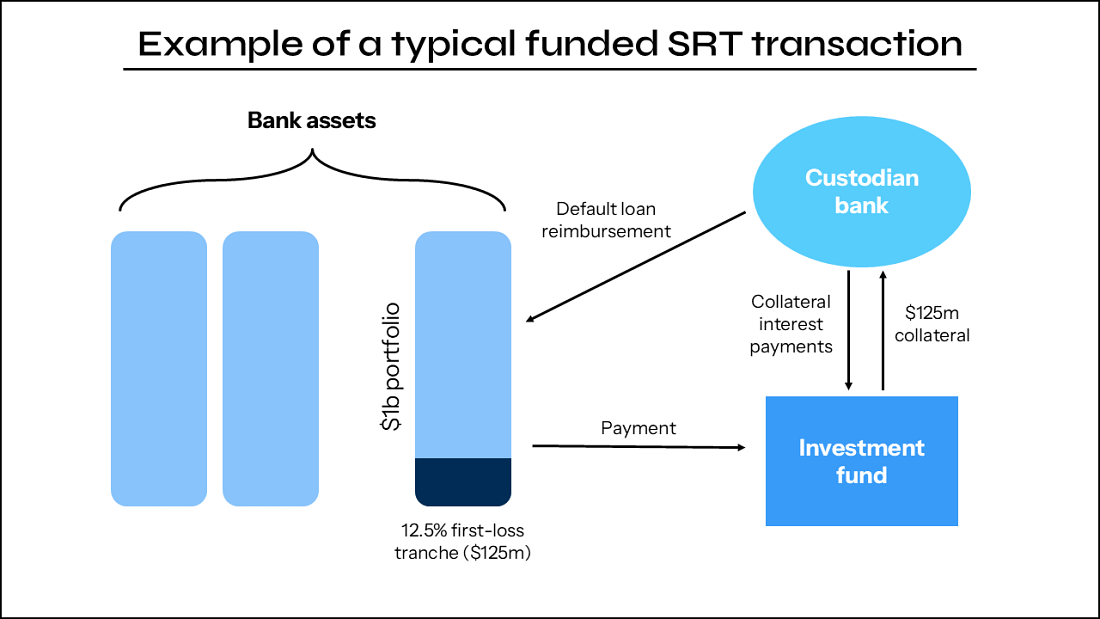

There was a warning sign before the crash, and it was hiding in plain sight. Silver ETFs were trading at persistent premiums to their net asset value. That means demand for ETF shares was so one-sided that the authorized participants whose job it is to create new shares and deliver physical metal couldn’t keep up. When the buying pressure outpaces the arbitrage mechanism, you’re not in a market anymore. You’re in a crowd. On the way down, these products turn into a machine that worsens crashes. Leveraged ETFs rebalance frequently, often daily, to maintain their target leverage. When prices fall, they have to sell silver to stay in balance. That selling pushes the price lower. The lower price forces more rebalancing. Which forces more selling… It’s a hamster wheel that only spins in one direction, and it’s bolted to a cliff. The BIS measured this using a “leverage rebalancing multiplier,” which tracks how much of the futures market these ETFs need to sell on a down day just to stay in balance. That multiplier doubled over the course of 2025. The mechanical footprint of these products was getting bigger and bigger, and nobody adjusted for it. Then three things happened at once. The leveraged ETFs started their automatic selling. Exchanges, seeing the volatility spike, raised margin requirements mid-crash... which forced leveraged futures traders to either post more cash or liquidate. And the smaller speculative investors who were long silver got margin called, dumping positions into a market that was already falling. The BIS describes what happened next as “a self-reinforcing loop of lower prices and further margin calls.” Silver recorded its largest single-day loss since the 1980s... falling about 30%. The BIS estimates that a drop of that size would require leveraged ETFs alone to sell roughly 3% of the entire silver futures market in a single day, just to rebalance. 4. Banks Are Paying Hedge Funds to Absorb Their Loan Losses (and Nobody’s Keeping Track)Consider the financial product called a synthetic risk transfer, or SRT. It allows banks to keep their loans but pay someone else to take the hit if those loans go bad. That sounds insane…

A hedge fund or private credit firm agrees to absorb the losses in exchange for a fee. The bank frees up capital and keeps lending as if the risk had disappeared. It’s like paying your neighbor to worry about your roof during a hurricane. Your house is still there. The hurricane is still there. But on paper, you feel great. This market has grown fivefold since 2016. Banks have transferred risk on nearly €800 billion in loans. And in the UK, just 10 firms sell protection, accounting for 60% of the market. If even one or two of those firms run into trouble, the protection can evaporate, and the risk can flow right back onto bank balance sheets. The BIS says these instruments could act as “transmission amplifiers” in a stress scenario… meaning they could freeze up bank lending right when the economy needs it most. And there’s no comprehensive central database tracking this market. The BIS itself warns that “SRT-related risks could build up undetected.” The last time someone told me the risk had been successfully transferred, it was 2007, and the guy saying it was the chairman of the Federal Reserve. About subprime mortgages. 5. Central Banks Have Gone Quiet Because They Don’t Know What to Tell YouThis one doesn’t come with a scary chart. It comes with something worse… silence. Back in the 2010s, most central banks provided some form of forward guidance on where interest rates were headed. Today, far fewer do, and many provide little to no forward guidance at all. No projections. No hints. Just… data dependence. Which is central banker speak for “we’ll figure it out when we get there.” That’s an insane strategy… right?

The post-COVID inflation surge proved that forward guidance can backfire badly. When a central bank promises rates will stay low and then has to jack them up because inflation explodes, the public feels betrayed. So now they just don’t promise anything. But the structural consequence is significant. If central banks aren’t telling you what they’re going to do, the market is no longer pricing policy signals. It’s pricing narratives… which can reverse on a single headline. The Common ThreadEvery one of these findings points in the same direction. The financial system is becoming more complex, opaque, and dependent on structures that no one fully understands. I had to spend a solid hour looking at a chart of how the hell an SRT works…

I’ve been using the wrong kind of scotch…

Every crisis in financial history starts the same way… somebody builds something clever, it gets very popular, and then one day everyone discovers that the pipes were connected in ways nobody had bothered to map. The BIS just handed you the blueprint. Learn it now… Stay positive, Garrett Baldwin About Me and the Money Printer Me and the Money Printer is a daily publication covering the financial markets through three critical equations. We track liquidity (money in the financial system), momentum (where money is moving in the system), and insider buying (where Smart Money at companies is moving their money). Combining these elements with a deep understanding of central banking and how the global system works has allowed us to navigate financial cycles and boost our probability of success as investors and traders. This insight is based on roughly 17 years of intensive academic work at four universities, extensive collaboration with market experts, and the joy of trial and error in research. You can take a free look at our worldview and thesis right here. Disclaimer Nothing in this email should be considered personalized financial advice. While we may answer your general customer questions, we are not licensed under securities laws to guide your investment situation. Do not consider any communication between you and Florida Republic employees as financial advice. The communication in this letter is for information and educational purposes unless otherwise strictly worded as a recommendation. Model portfolios are tracked to showcase a variety of academic, fundamental, and technical tools, and insight is provided to help readers gain knowledge and experience. Readers should not trade if they cannot handle a loss and should not trade more than they can afford to lose. There are large amounts of risk in the equity markets. Consider consulting with a professional before making decisions with your money.

|

Subscribe to:

Post Comments (Atom)

0 Response to "Five "WTF Moments" from the BIS Quarterly Review"

Post a Comment