If you are watching gold, you know the price action has been historic. Gold rose 239% from its low in 2022 – and then dropped 16% in a single day.

What I’m watching is why.

Here’s what’s going on behind the scenes in gold:

As usual, the mainstream press is late. Here’s Bloomberg… from late January 2026.

“Tether Is Shaking Up the Gold Market With Massive Metal Hoard”

Now, none of this is news to me – or my readers…

Back in September, I attended a private dinner at a ski resort in Beavercreek, Colorado.

At that meeting was the who’s who of the gold world:

- Randy Smallwood, CEO of Wheaton Precious Metals…

- Paul Brink, CEO of Franco-Nevada…

- Fred Bell, CEO of Elemental Royalties…

- And me

You can go here to read all about it.

But the man we were all there to listen to was the head of special projects for crypto whale, Tether.

Why?

Because Tether is already the largest private owner of gold in the world…

And they are buying gold at a pace that makes institutional investors blush:

Tether is buying roughly two tonnes of gold – per week… and they don’t care about price.

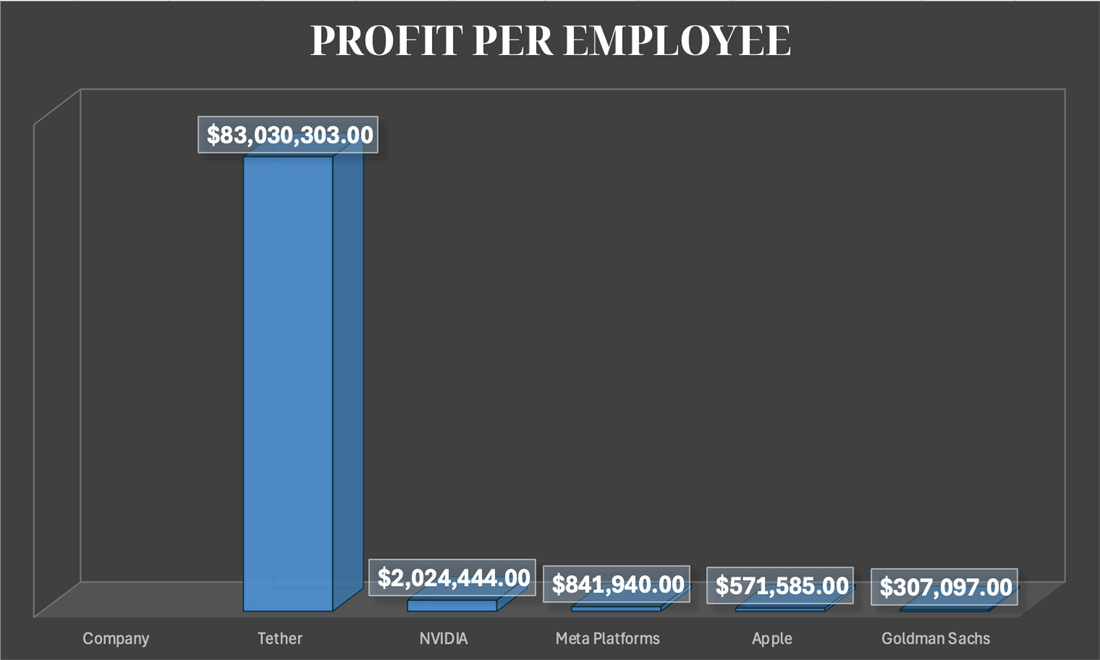

If you don’t know Tether, they are the biggest whale in the crypto world. Their USDT stablecoin is worth roughly $190 billion.

Tether has an almost unbelievable business model…

They create a crypto “asset” from thin air… back it with US Treasuries – pocketing the interest (3-4%)… and have less than 200 employees.

Tether boasts a profit margin of 99% – roughly $90 million for each employee – making it far and away the most profitable company in the world.

So, why should you care?

Tether has the explicit backing of the US government. More importantly…

In 2025, they reported $13 billion in profits. And here’s why I’m telling you this:

They’re using those profits to buy the world’s most trusted form of real money: gold.

So, let me ask you this…

If Tether is quite literally printing billions in profits… has the backing of the US government… and is now using those profits to buy gold…

What should you be buying? Now…

You can go buy gold at these prices – but I wouldn’t recommend it. The time to buy physical gold was in 2022 before it ripped higher. But that’s okay…

Because there’s a better way to own gold.

If you want all the details about my meeting with Tether’s head of special projects – including for top miners poised for gains of 10X–50X… Go here to read more.

Best,

Garrett Goggin, CFA, CMT

Lead Analyst and Founder, Golden Portfolio

P.S.

Notice the date on the post above – January 28, 2026. As usual, social media “experts” are painfully late. Back when I broke this Tether story in September 2025, gold was still trading below $3,500 an ounce. Since then, it’s up over 60%.

Better yet, my top four miners are up 202%... 540%... 744%... and 1,551% in just the last two years. Go here to find out how I pick the only gold miners you want to own for the coming gold bull mania.

Wendy's Is Down Sharply—Is the Dividend a Bargain or Value Trap?

Author: Chris Markoch. First Published: 3/1/2026.

Key Points

- Wendy’s shares remain under heavy pressure despite a Q4 earnings beat, driven by the company’s worst same-store sales performance in two decades.

- Management is pursuing store closures, menu value initiatives, and the “Project Fresh” overhaul as it navigates a strained lower-income consumer.

- A 7%+ dividend yield may attract income investors, but weak growth guidance and declining free cash flow raise concerns about a value trap.

- Special Report: Elon Musk already made me a "wealthy man"

The Wendy’s Co. (NASDAQ: WEN) delivered a double beat when it reported Q4 2025 earnings on Feb. 13. Still, shareholders lost their appetite for WEN stock, which fell to a 52-week low of $6.73. Recent headlines helped the stock rally, but it remains down nearly 51% over the last 12 months and more than 61% over the last five years.

Big numbers worked against the company: Wendy’s posted its worst same-store sales performance in 20 years. That’s hard for shareholders to overlook.

Silicon Valley Bank was just a warning (Ad)

In 2023, Silicon Valley Bank collapsed in just 48 hours with panicked customers draining $42 billion in a single day, but it could be nothing compared to what's coming next—through Federal Reserve Docket No. OP-1670, the government is rolling out FedNow, an instant 24/7 payment hub that over 1,500 banks have already connected to, and when money moves at the speed of light, a modern bank run won't take days. By routing every transaction through a single centralized hub, the Fed is building the ultimate kill switch for the American banking system, and when the next financial crisis hits, the Federal Reserve could instantly freeze all transfers, withdrawals, and payments nationwide to protect the system, trapping your life savings inside.

Get the 4 steps to Fed-proof your savings nowBut has the stock become so beaten up that it’s attractive? As with many retail stocks, value often depends on the viewer. Hedge fund billionaire Nelson Peltz appears to see opportunity. Peltz has been a major shareholder for more than two decades and has been evaluating ways to boost shareholder value. An SEC filing indicated that one option could be a takeover of the fast-food chain.

Wendy’s is already undergoing a transformation under Project Fresh and plans to close between 5% and 6% of its locations in 2026. The company has also adjusted its value menu (i.e., the Biggie Bag) to be more competitive.

It’s unclear what additional value Peltz might unlock; one possibility is helping the company land a permanent chief executive officer — the company is currently led by interim CEO Ken Cook. For now, it’s useful to evaluate the stock on its current fundamentals.

Turnaround Efforts Face Macro and Consumer Headwinds

The fact that Wendy’s beat both top- and bottom-line expectations was legitimately better-than-expected, not just better-than-feared. Still, the steep drop in same-store sales is difficult to ignore.

Interpretation is the challenge. Investor outlooks vary widely depending on which segment of the so-called "K-shaped" economy you focus on.

Lower-income consumers are under pressure. If the debate centers on which $5 value meal delivers the most "value," the problem may lie more with the consumer than the company.

Add concerns about GLP-1s, and it’s reasonable to conclude Wendy’s may be doing about as well as can be expected under the circumstances. This was a $20 stock in 2021 — but that was then.

Wendy’s is forecasting relatively flat global sales growth and adjusted earnings per share (EPS) between $0.56 and $0.60, which would represent about a 32% decline if the company hits the high end of that range.

The company is trimming capital expenditures by roughly $10 million to $20 million and expects free cash flow (FCF) to fall to $190 million from $205 million.

Those projections carry a "more of the same" bias, which may be prudent: 2026 looks like a year in which a range of outcomes for the lower leg of the K are possible.

A Tasty Dividend or Value Trap?

One bright spot for WEN stock is its dividend.

The payout was slashed nearly in half in 2025 but still stands at $0.56 per share. With the stock trading around $7.70 as of this writing, that equates to a yield of about 7.26%.

Whenever a dividend yield looks attractive after a weak report, investors rightly ask whether the payout is sustainable — especially given the decline in free cash flow.

At current levels the dividend costs Wendy’s about $106 million annually, which appears sustainable even with the forecasted drop in FCF.

The payout ratio is higher than ideal at roughly 65.9% (investors generally prefer something below 50%), but there’s no immediate indication the dividend is unsafe based on the company’s conservative guidance.

Technical Picture Suggests Rally May Be Temporary

WEN stock has been in a persistent downtrend since March 2025, falling from roughly $16 to around $7.73 and tracking the lower Bollinger Band for months. Price currently sits near the 20-day simple moving average (about $7.82), which has acted as resistance throughout the decline rather than support.

After the sharp February sell-off and subsequent bounce, the stock has mean-reverted to the middle Bollinger Band. That suggests the oversold condition created by the pullback has already been relieved and that the recent recovery was corrective rather than the start of a durable reversal.

The moving average convergence/divergence (MACD) supports this view. While the MACD line briefly crossed above zero during the bounce, it’s rolling back over and the signal line remains deeply negative (-0.1239). Resistance at the upper Bollinger Band (around $8.41) remains a significant hurdle; without convincingly reclaiming that level, the path of least resistance still points lower.

3 Stocks Sending a Strong Signal With Massive Buybacks

Author: Leo Miller. First Published: 3/9/2026.

Key Points

- Cheniere, Fair Isaac, and Zillow all expanded buyback authorizations, signaling confidence and a stronger commitment to capital returns.

- Cheniere stands out for the sheer scope and duration of its repurchase capacity, giving it unusually large flexibility to shrink the share count over time.

- Fair Isaac is leaning on buybacks as shares digest policy-related headlines, while Zillow is using repurchases to capitalize on a depressed share price amid housing and regulatory uncertainty.

- Special Report: Elon Musk already made me a "wealthy man"

Three leading stocks across their industries have just announced substantial buyback programs. One energy company now has repurchase capacity nearing 20% of its market capitalization, giving it significant flexibility to return capital to shareholders. That company, along with two others, is signaling strong confidence through these latest buyback moves.

LNG Plans +$10 Billion in Buybacks Through 2030

Cheniere Energy (NYSE: LNG) is one of the world's largest exporters of liquefied natural gas. The company acts as an intermediary, taking natural gas from producers, liquefying it, and then finding buyers. Liquefied natural gas is a key and growing part of the global natural gas market. Liquefaction enables transportation of the gas on ships or trucks, rather than by pipeline, so buyers and sellers can connect even if they are on opposite sides of the world.

Silicon Valley Bank was just a warning (Ad)

In 2023, Silicon Valley Bank collapsed in just 48 hours with panicked customers draining $42 billion in a single day, but it could be nothing compared to what's coming next—through Federal Reserve Docket No. OP-1670, the government is rolling out FedNow, an instant 24/7 payment hub that over 1,500 banks have already connected to, and when money moves at the speed of light, a modern bank run won't take days. By routing every transaction through a single centralized hub, the Fed is building the ultimate kill switch for the American banking system, and when the next financial crisis hits, the Federal Reserve could instantly freeze all transfers, withdrawals, and payments nationwide to protect the system, trapping your life savings inside.

Get the 4 steps to Fed-proof your savings nowS&P Global notes that liquefied natural gas imports to Europe surged 30% year-over-year (YOY) in 2025, with the United States supplying over 77% of those imports. Over the past five years, Cheniere Energy shares have benefited from strong demand, rising more than 250%. The energy stock fell significantly in the second half of 2025 but has rebounded strongly in 2026 and is now near its all-time high.

Demonstrating conviction in its outlook, Cheniere bought back $2.7 billion worth of shares over the last 12 months (LTM), its largest total ever. The company plans to continue buying back shares at a strong pace, recently boosting its buyback capacity to $10.2 billion — roughly 20% of its approximately $52 billion market capitalization. The firm called the move a "clear mark of confidence," and it gives Cheniere the ability to materially reduce its outstanding share count through 2030.

FICO: Financials and Buybacks Are Up as Shares Fall

Fair Isaac (NYSE: FICO) is the dominant U.S. provider of consumer credit scores. The company's FICO Score is often the de facto metric for assessing risk when financial institutions offer loans, from mortgages to credit cards. The market has hit FICO shares fairly hard over the past year: the stock is down roughly 30% from its 52-week high, reached in May 2025.

A large part of the stock's decline stemmed from actions by the Federal Housing Finance Agency (FHFA). FHFA Director Bill Pulte criticized the company's price increases for mortgage application credit scores, which pushed shares lower. The FHFA then removed the requirement for loans purchased by Freddie Mac (OTCMKTS: FMCC) and Fannie Mae (OTCMKTS: FNMA) to use the FICO score, a direct challenge to Fair Isaac's dominance.

Despite that pressure, Fair Isaac has maintained solid growth and improved profitability. Revenue has risen by 13% or more year-over-year in each of the last four quarters, and the company's adjusted operating margin increased by over 300 basis points in fiscal 2025.

With its shares depressed, Fair Isaac has boosted buybacks substantially. The firm spent more than $1.5 billion on repurchases in the LTM, near its highest five-year level. It recently announced a $1.5 billion buyback authorization, equal to about 4.3% of its roughly $35 billion market capitalization. That gives the company considerable capacity to repurchase shares at prices it likely views as attractive.

Zillow's Buyback Capacity Exceeds 10% With Shares Down Big

Next up is Zillow Group (NASDAQ: ZG), known for its leading platform that connects home buyers and renters with sellers and landlords. Zillow shares have been hit hard in the past six months, falling more than 45% from their 52-week high. A variety of factors contributed to Zillow's weakness, including a softer housing market and an ongoing investigation by the Federal Trade Commission.

The FTC alleges that Zillow and Redfin illegally stifled competition after Zillow paid Redfin $100 million to re-host its rental listings, making many of the two companies' listings identical. The FTC argues this was anti-competitive; Redfin says the deal was necessary because a lack of paid independent listings made operating its sales force uneconomical.

Still, Zillow delivered solid revenue growth of 15% in 2025 and saw its operating margin improve materially. The company has sharply increased buyback activity in 2026, spending $626 million on repurchases through early March — nearly as much as the $670 million it repurchased in all of 2025.

Now, Zillow has replenished its buyback capacity, boosting its repurchase authorization to $1.3 billion. That represents more than 11% of its roughly $11 billion market capitalization and gives the company significant leeway to buy back shares. During its February earnings call, Zillow said it was taking advantage of the "recent market dislocation to buy back shares at what we believe is an attractive price."

Zillow Stands Out for Its Upside Potential

Overall, these three companies are giving investors reason to take notice with their buyback programs. Among them, analysts see the most upside in Zillow. The MarketBeat consensus 12-month price target of about $78 implies roughly 66% upside. That said, price targets were revised down materially after the company's latest earnings report.

to bring you the latest market-moving news.

This message is a sponsored message provided by Golden Portfolio, a third-party advertiser of TickerReport and MarketBeat.

Contact Us | Unsubscribe

© 2006-2026 MarketBeat Media, LLC dba TickerReport.

345 North Reid Place, Sixth Floor, Sioux Falls, S.D. 57103. USA..

0 Response to "Tether is moving the gold market… (just like I predicted)"

Post a Comment