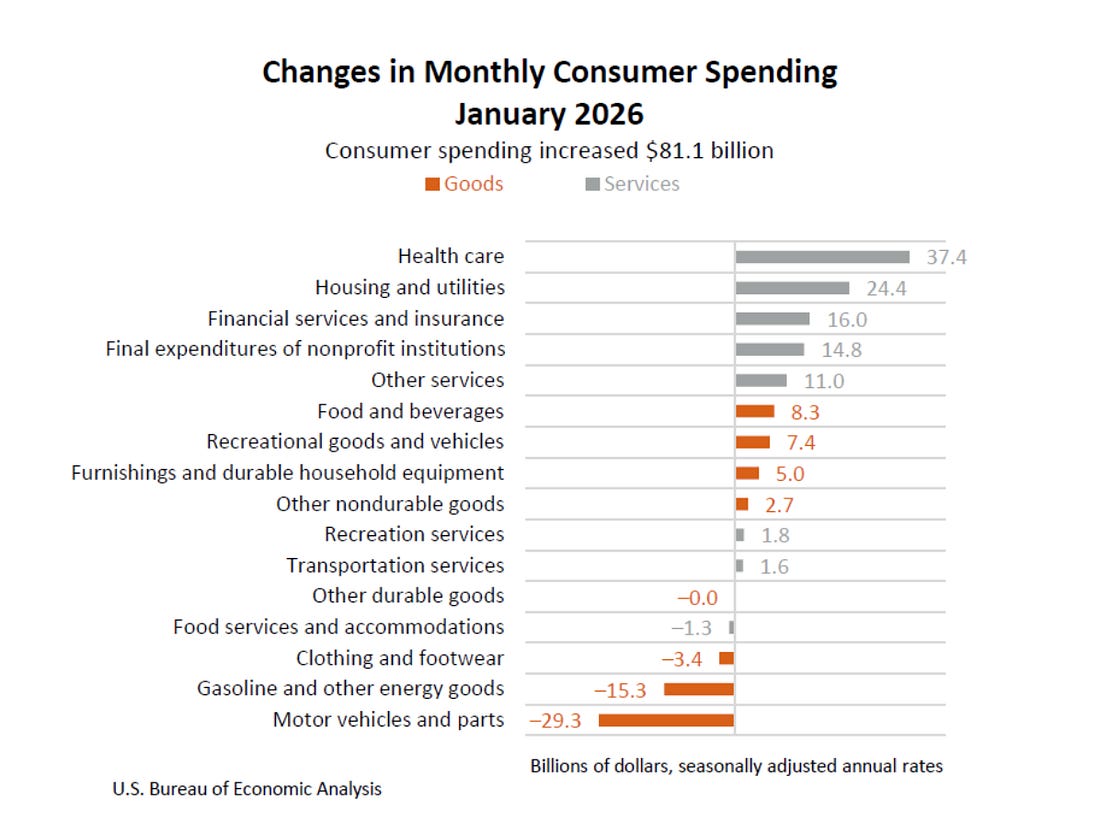

To Whom It May Concern (You): On March 13, 2026, the Bureau of Economic Analysis released its Personal Income and Outlays report for January. That’s a fancy way of saying the PCE Index, or the Fed’s preferred measure of inflation. Now, they massage this number so tender it should offend most of us… But the reality is that even in the face of damned lies and statistics, the figures still scream something about the state of monetary debasement. The headline was familiar. Personal income increased by 0.4%. Consumer spending added 0.4% too. And core PCE inflation is still running above the Fed’s 2% target. But the chart underneath the headline told the real problem with our economy...

Of the $81.1 billion increase in consumer spending that month, $37.4 billion went to healthcare services. That was about 46 cents of every new dollar Americans spent. It wasn’t put toward building wealth, buying homes, feeding the belly, or taking a trip. It went to the greatest extraction sector of them all… U.S. healthcare. Now, this is not an advocacy argument… It’s not a policy paper. It’s just a dive into the numbers, and where Americans’ money (and thus time) is being allocated in the broader world of their spending. On the other side of the ledger… spending on motor vehicles fell by $29.3 billion. Gasoline fell by $15.3 billion. Clothing dropped $3.4 billion. Restaurants fell by $1.3 billion. Healthcare absorbed nearly half of the increase in consumer spending that month. You think this is a responsible system? You think this is sustainable? It’s the ultimate extraction vehicle. This wasn’t a burst of consumer desire. It was a forced payment. Nobody woke up in January and decided to spend less on food so they could spend more on medical care… NO ONE.

The Ways They TakeThe U.S. spends more on healthcare than any country on earth… In 2024, national health expenditures reached $5.3 trillion… or 18% of GDP… That’s incredibly insane. That’s roughly $15,000 per person. The next-highest spending nation was Switzerland. Their annual spending came in at around $9,300 to $10,000 per person, and that’s a place where we can really call healthcare a service… and not a product. The OECD average is closer to $5,500. So, the U.S. spends about 2.5 to 3 times the OECD average. Do we immediately see the problem here? Not yet… Well, here’s the punchline. For that price, Americans live shorter lives. U.S. life expectancy was 78.4 years in 2023, but still trailing peer high-income nations by roughly three to four years. The U.S. infant mortality rate is WELL higher than in Japan, Norway, and Sweden. The U.S ranks near the bottom of OECD countries in infant mortality… and first in spending. Well done, everyone. The most expensive healthcare system in history produces outcomes worse than those of countries that spend less than half as much. That’s the definition of a grift… Healthcare spending has grown faster than GDP, wages, and inflation for decades. In 2000, total spending was $1.4 trillion. By 2024, it was $5.3 trillion. By 2033, CMS projects it will reach 20.3% of GDP. One in every five dollars the American economy produces will flow through the healthcare system. And the system has no structural incentive to slow down… Because every layer of it is fueled to scale as costs rise. What’s Beneath the NoiseLet’s look at the architecture… and the massive policy mistake it caused. Under the Affordable Care Act, health insurers are required to spend at least 80% to 85% of premium revenue on medical care. This is called the “medical loss ratio.” If they don’t hit the threshold, they owe rebates. You know what a bunch of companies don’t want to do? Pay money back… It sounds like consumer protection, but it’s just another joke. If an insurer must spend 85 cents of every premium dollar on care, its non-medical spending, including profit, is capped at roughly 15% to 20% It sounds like the government is “doing something.” But 15% of a large number is more than 15% of a small number. So the incentive is not to reduce costs. It’s to let costs rise… and raise premiums to match. The absolute profit grows every time the underlying cost of care increases. This is just math linked to incentive structures. The same arithmetic made Wells Fargo’s fines irrelevant in Volume 15 of Postcards. The system is not designed to reduce extraction. It’s designed to manage it at a sustainable rate… with the hope that fewer people complain and throw up their hands in defeat. And if you need to really see it in action, look at the vertical integration model… The three largest pharmacy benefit managers… CVS Caremark, Express Scripts, and OptumRx… control roughly 75% to 80% of prescription drug claims in the nation. All three are owned by vertically integrated healthcare conglomerates with major insurance operations. UnitedHealth owns OptumRx. Cigna owns Express Scripts. CVS owns Aetna and Caremark. Under that scenario, the insurer sets the premium. The PBM negotiates the drug prices, and pharmacies fill the prescription. In many cases, all three are the same company. How brilliant… no one notices the extraction in action. It’s all one big laundry machine. The “negotiations” we hear about regarding pricing are really internal transfers. Most rebate savings never reach the patient at the pharmacy counter. And the medical loss ratio counts payments to affiliated subsidiaries as “medical expenses,” which means the 85% rule can be satisfied without 85 cents actually reaching your care. Three companies sit in the middle of most prescription drug claims in America. And they own the insurers who are supposed to be negotiating on your behalf. Congratulations, America. You voted for this...

How Power Really WorksIn Volume 15, I named the enforcer… the regulator who “manages” misconduct rather than ending it. Healthcare has the same architecture, but the enforcer is harder to see because it’s woven into the tax code. The exclusion for employer-provided health coverage amounts to $240 billion to $300 billion in annual tax subsidies in 2026. It’s almost cartoonish how much we fire out of a cannon at healthcare… Your employer’s contribution to your health insurance is tax-exempt. It doesn’t show up on your W-2 as income. That sounds like a benefit… until you realize what it actually does. Now… listen. This is important, and a lesson in how extraction really works. It hides the real price of healthcare from the person paying for it. Your family coverage may cost roughly $27,000 per year, with the employer paying most of it. You see a payroll deduction, and you’re convinced your healthcare costs a few hundred dollars a month. But it really costs over $2,000 a month. The subsidy doesn’t reduce the price. It obscures it. And because you never see the real number, you never revolt against it. That’s the whole point… The extraction mechanism is not the insurance premium itself. It’s the invisibility of the insurance premium. The healthcare system now absorbs $5.3 trillion a year from the American economy, and the primary reason it survives is that most Americans have no idea what they’re actually paying… or for what… Meanwhile, hospital chargemaster prices often show no real relationship to underlying costs, and some departments have historically posted markups exceeding 20 times cost. The chargemaster… the internal price list every hospital maintains… exists to create a starting point for “negotiation” with insurers. The negotiated price is presented as a discount. The patient feels like they got a deal. A hospital might bill $40,000 for a procedure, the insurer negotiates it down to $22,000, and everyone congratulates themselves on the savings. It’s seriously a joke. The patient never learns that the same procedure may cost dramatically less in peer countries. And I’m not talking about Mexico, where there is foolishly some bias against the doctors. I’m talking about advanced medicine in Switzerland and Germany. The Everyday HustleMedical debt affects tens of millions of Americans. The total owed is at least $200 billion, according to the American Medical Association. Medical bills and illness-related income loss are a major driver of household financial problems… even if the exact share of bankruptcies tied to health costs is debated, the weight of the evidence is staggering. Remember… these aren’t irresponsible people. Most Americans did everything right… They had insurance, went to an in-network provider, followed the rules… and still got a bill that broke them. On HealthCare.gov marketplace plans, insurers denied 19% of in-network claims and 37% of out-of-network claims in 2023. Remember… this was the marketplace that was supposed to ensure coverage… this was the hallmark of government-sponsored healthcare. And it still showed us the reality of the system. But here’s the funny thing about our system… Fewer than 1% of denied in-network marketplace claims were appealed. Of those appeals, 44% resulted in the denial being overturned. In Medicare Advantage, prior authorization, more than 80% of appealed denials were overturned. That’s an insane reversal rate. So… this medical system denies plenty of claims that would likely be paid if challenged, and it benefits from the fact that very few people appeal. The denial isn’t a medical decision. The whole system is based on a wager… It operates on a bet that you’ll pay the bill, absorb the cost, or simply give up. And 99 times out of 100, the bet pays off. People don’t know any better… That’s extraction at the individual level. But the macro picture is worse. Go back to that January PCE report. In that month, healthcare absorbed about 46% of new consumer spending. That means every other industry in the American economy… restaurants, retailers, automakers, clothing brands… is competing for the 54 cents that healthcare didn’t take. When healthcare spending crowds out discretionary income at this scale, it doesn’t just hurt households. It starves every other sector of the economy. Nearly half of all new consumer spending in January flowed into healthcare alone. Motor vehicles saw a $29.3 billion decline, while healthcare absorbed an outsized share of new consumer spending. We can’t just be a healthcare economy. You can’t live off gauze… The Real EconomyHealthcare spending as a share of GDP… Thanks a lot, Nixon. It was 5% in 1960. 13% in 2000. 18% in 2024. It’s projected to exceed 20% by 2033. That trend line has been relentlessly upward over time, regardless of the president… It doesn’t change depending on Congress, reform efforts, or economic conditions. It survived the managed care revolution of the 1990s. It survived the comically named ACA… and, of course, COVID. And it’s full speed ahead now. Healthcare spending grew 7.2% in 2024, the fastest increase in more than a decade, far outpacing nominal GDP growth. Every year, healthcare captures a larger share of the economy… which means every year, less is left for wages, savings, investment, and the things that actually build household wealth. The personal saving rate hovered around 5% at the start of 2026. The Debasement Index, which I explained in Volume 11, expands by at least 6.7% per year. Americans are saving at a rate that loses purchasing power before healthcare takes its cut. After healthcare takes its cut, the math gets even worse. The system that was supposed to keep people healthy is the single largest force preventing Americans from building wealth. It grows every year regardless of who’s in charge… because the incentives point in only one direction. What’s worse… the people running this thing - from the policymakers to the pillagers at the heavily controlled insurance industry… They don’t care. They’re probably buying new boats as we speak. The Back PageThere’s a pattern that runs through the American economy, and once you see it, you can’t unsee it. The sectors where prices fall over time… consumer electronics, software, televisions, computing power… share one trait. They operate in intensely competitive markets where consumers can easily compare prices. Technology is deflationary by nature. A television that cost $5,000 in 2005 costs $400 today and has a better picture. A smartphone in your pocket has more computing power than the machines that landed Apollo 11. Competition and innovation push prices down. That’s what markets do when they’re allowed to function. Now look at the sectors where prices rise faster than inflation, year after year, decade after decade. Think… healthcare, education, housing in regulated markets, electricity, and food. What do they share? Government subsidies, federal loan guarantees, and tax exemptions. They have regulatory frameworks that protect incumbents from competition and guarantee demand regardless of price. This is not a left-right, Liberal-Conservative, Democratic-GOP observation. It’s an up-or-down one… sink or swim. The subsidies don’t reduce costs. They remove the market signals that would. When the government guarantees student loans regardless of tuition price, tuition rises. When the government subsidizes health insurance premiums through employer tax exclusions, premiums rise. When the government guarantees mortgage liquidity through Fannie and Freddie, housing prices rise. How is this so hard? The subsidy doesn’t lower prices. It weakens the price signal that would… and it removes the one force that has ever reliably reduced prices in human history. Competition. We throw past, present, and future money at the problem. I don’t think these people in charge are this stupid. They’re just motivated by money and power… And they park themselves in the center of all of it… because it’s a constant need. Healthcare is the purest expression of this pattern. It was 5% of GDP in 1960… before Medicare and Medicaid reshaped the system in 1965. The more the government subsidizes, the more the system extracts. And the extraction never reverses… because the subsidy guarantees there will always be someone to pay… regardless of the damage. The longest invoice in American life isn’t your mortgage. It isn’t your student loans. It’s the healthcare bill that starts the day you’re born, compounds every year faster than your income, and never arrives in a single envelope… because the system was designed to spread it across premiums, deductibles, copays, taxes, and prices you never see. You pay it for your entire life. And most people never add it up.

Your Sovereign Moves (Household)Each week, I provide moves you can do at home, regardless of how much money you have or whether you can afford to invest in the extraction. Here are things you can do to take back your time and money. 1. Learn your actual healthcare cost. I’m not talking about your payroll deduction. I mean, your total cost. Ask HR for the full premium your employer pays on your behalf. Now, add your deductible, copays, out-of-pocket max, and prescriptions. Most families will find the real number is $15,000 to $25,000 per year. You can’t negotiate what you can’t see. 2. Appeal every denial. Yes, appeal. Always. About 44% of appeals succeed. The system bets you won’t fight. You need to fight. If a claim is denied, file a written appeal within 30 days. If the internal appeal fails, request an external review. The insurer is required by law to provide one. Seriously, bury these people in paperwork. By the time you might be done with them, they might end up spending as much money trying to defend your appeal as the cost of just paying the damn bill would have been. 3. Use the hospital’s price transparency data. Since 2021, hospitals have been required to publish pricing data online, and the 2026 rules expand those disclosures. Most hospitals bury the files. Find them and compare prices before procedures when possible. 4. Investigate direct primary care. DPC memberships often run roughly $60 to $120 a month for an adult. They include unlimited primary care visits, basic labs, and generic prescriptions. There is no insurance middleman, copays, or claim denials. Beginning in 2026, certain direct primary care arrangements can remain HSA-compatible, subject to monthly fee caps of roughly $150 per individual and $300 per family. Pair a DPC membership with a high-deductible plan and an HSA for catastrophic coverage… and you’ve stepped outside the extraction system for most of your routine care. 5. Max out your HSA. This is the single most important financial tool inside the healthcare extraction machine… and almost nobody uses it correctly. If you have a high-deductible health plan, a Health Savings Account offers something no other account in the American tax code provides. Contributions are pre-tax, and growth is tax-free. Withdrawals for medical expenses are tax-free. It has a triple tax advantage. No 401(k), no IRA, no brokerage account offers all three. The 2026 contribution limit is $4,400 for individuals and $8,750 for families. Fund it fully every year. Invest it for growth. Pay current medical expenses out of pocket if you can, and let the HSA compound. Over a working lifetime, a fully funded and invested HSA can grow into a six-figure tax-free medical reserve… which means you are building wealth inside the same system that is designed to extract it from you. That’s the free sovereign move. The one that costs you nothing but attention.

The Sovereign MoveThe HSA is how you defend yourself. This is how you position yourself on the other side of the extraction. Healthcare spending has marched higher for decades, and its share of the economy keeps rising… under every president, through every reform, in every economic condition. That means the institutions that deliver healthcare will always have revenue. And the buildings where that healthcare is delivered will always have tenants. If you can’t beat the extraction machine, own the building it operates in. Each week, I offer an investment idea… for paid subscribers. The HSA opportunity will do you well… but if you want the latest investment idea and you want to help support Postcards, please consider a subscription. I’ve made it very easy for you today…Once you’ve joined, click this link to get the idea… Stay positive, Garrett Baldwin About Postcards from the Edge of the WorldThe Postcards Doctrine holds that wealth, power, and stability do not persist through innovation, morality, institutions, or financial sophistication, but through control of chokepoints that remain productive across regime change. Civilizations rise and fall. Ideologies rotate. Technologies obsolete themselves. Financial instruments are rewritten, repudiated, inflated away, or nationalized. What survives is not what performs best in good times, but what continues to function when systems fail, rules change, and authority resets. The doctrine begins with a simple observation: extraction always migrates toward what people cannot avoid. Early on, extraction flows through trade. Then finance. Then regulation. Then platforms. Then metered access. Eventually, it settles on inputs that cannot be substituted, deferred, or digitized. Postcards are sent from the edge of these transitions. Each one documents a moment when the system tightens, when optionality narrows, and when value stops flowing to innovation and starts flowing to ownership. Enjoy.

|

Subscribe to:

Post Comments (Atom)

0 Response to "The Longest Invoice Is Still Unpaid..."

Post a Comment