Can you believe I was buying Amazon and Apple in February while the market chopped…

Then, when the first bombs hit Iran, I got out.

Geopolitical conflicts are tough on tech stocks.

Sure, I still got out with gains on Amazon and Apple… but the key is I got out at the exact right time.

My name’s Scott Redler. I’m a certified professional trader for over 30+ years… I have over 200k followers online.

Right now, there’s little to buy.

But, you’ll know when to start buying.

Just use my #1 indicator. It’s free and you can use it on your chart right now.

I’ve used it for 30 years… and it’s helped me get out before the Covid drops, the 2022 bear market, and get back in when assets like Bitcoin start ripping (like it did in 2024).

You can get a breakdown of my indicator on the next page…

Plus, I’ll also give you my bi-weekly weekly report on what the stock market is doing each week and my watchlist for those days.

This is a tough market to buy in…

Add this indicator to know when you can size up your positions,

Scott Redler

Co-Founder of T3 Live & Editor of Power Plays

Disclosures

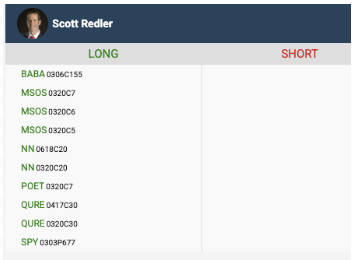

Scott Redler Positions Disclosure as of 2026-03-03 at 10.14.38 AM

These are not Power Plays ideas.

Is the Airline Stock Dip After the Iran Attacks Justified?

By Nathan Reiff. Originally Published: 3/10/2026.

Key Points

- Many airline stocks have plummeted by 20% or more in the last month amid the start of war in Iran and related oil price volatility.

- Airline companies face numerous negative pressures related to the war, including canceled flights, the potential for suppressed demand, and more.

- Jet fuel prices and cracks have spiked, meaning that even airlines not doing business within the area of conflict will feel the repercussions.

- Special Report: Elon Musk already made me a "wealthy man"

As the war in Iran appears likely to continue, it's no surprise that airline stocks have been among the first to feel a significant impact. These shares are closely tied to fuel costs, geopolitical stability, and consumer demand—all three have grown increasingly erratic as the conflict escalates and spreads. Both major carriers and smaller domestic and regional names have seen sharp declines: Delta Air Lines (NYSE: DAL) and American Airlines Group Inc. (NASDAQ: AAL) have dropped by about 22% and 27%, respectively, over the past month.

For investors, the price decline may present an opportunity to add to positions in the airline industry. But it's important to weigh whether the war's initial shock—and the associated oil-price worries—justify the selloff, given airlines' recent domestic resilience. If the conflict prolongs and further pressures shares, waiting to enter or build a position may be prudent.

Major Air Carriers Face Multiple Negative Drivers

The table went quiet… [my meeting with Tether Gold] (Ad)

A major force in the crypto world is quietly becoming one of gold's most aggressive buyers — and most investors have no idea it's happening.

A longtime gold analyst says profits from a leading stablecoin operation are being funneled into physical gold at a scale that could materially impact supply and demand. After a recent meeting with insiders, he began outlining what this trend could mean for gold prices and a small group of companies positioned to benefit.

Delta, American, and other major airlines have fared particularly poorly since the start of the war because several negative factors have converged.

First, thousands of commercial flights to and from parts of the Middle East have been canceled, creating operational and logistical costs for carriers while reducing revenue opportunities.

Second, and perhaps most consequential, jet-fuel costs have surged. The Argus US Jet Fuel Index rose to $3.88 on March 6 from $2.50 a week earlier. While crude oil has been volatile since the conflict began, refined petroleum products have seen even greater stress. Jet-fuel prices and cracks—the differential between crude oil and the jet fuel refined from it—have widened substantially.

Finally, consumer demand is an uncertain but worrying factor. In its most recent earnings report, Delta said it remained optimistic about demand despite the government shutdown, pointing to loyalty and cargo growth and improvements in non-ticket revenue. Similarly, fellow Big Four member United Airlines (NASDAQ: UAL) reported in its Q4 2025 report its highest-ever seat completion factor and a 12% year-over-year increase in premium revenue.

However, if consumers brace for higher gasoline prices and broader inflation from oil-market volatility, discretionary leisure travel could decline as households redirect spending to essentials. The impact on airline demand may be delayed, but it could persist even after transport and inventory issues settle.

Can Regional Airlines Fare Any Better?

Even airlines that don't operate in the Middle East or that focus on domestic routes are being affected, largely because fuel is a major input across the industry.

One modest bright spot is Air Canada (TSE: AC), whose shares have fallen only about 13% in the last month. Still, that decline is meaningful and hardly a vindication of the sector.

Some Wall Street analysts have already adjusted expectations: since the start of the month, for example, Weiss downgraded DAL to Hold from Buy, and other firms have trimmed price targets. Investors may opt to wait for further weakness before committing capital.

Watching short-interest trends can also help gauge market sentiment. Companies such as American were already seeing rising short interest before the conflict began, which could intensify if downside pressure continues.

Ultimately, how much further airline shares fall depends on the duration and scope of the conflict. If tensions persist or widen, early 2026 could start to feel eerily similar to early 2020, when COVID-19 effectively grounded the industry. To reach those lows would require substantially larger declines than we've seen so far, so bearish investors may prefer to wait and see how low airline stocks will fly.

AeroVironment Touches Down On Value Opportunity

By Thomas Hughes. Originally Published: 3/12/2026.

Key Points

- AeroVironment faces near-term pressure from the SCAR contract ending, but analysts still see meaningful upside from current levels.

- AVAV’s chart suggests a possible hard bottom near $200, with key resistance levels at $225, $240, and $250.

- Strong institutional ownership and continued contract execution and scaling efforts could help restore momentum in 2026.

- Special Report: Elon Musk already made me a "wealthy man"

AeroVironment (NASDAQ: AVAV) faces headwinds in 2026, including the end of its SCAR contract and the resulting impact on market sentiment. Even with analysts trimming targets and guidance coming in below expectations, this defense company still presents value for investors willing to buy at long-term lows and wait for recovery. It remains well-positioned with a battle-proven product portfolio, a solid—if reduced—backlog, and a healthy balance sheet that supports reinvestment and potential shareholder-value initiatives. The primary question is timing: a rebound could arrive sooner than the guidance update implies.

Analysts are trimming targets following the fiscal Q3 2026 earnings update, but that is the most negative takeaway from the report.

The table went quiet… [my meeting with Tether Gold] (Ad)

A major force in the crypto world is quietly becoming one of gold's most aggressive buyers — and most investors have no idea it's happening.

A longtime gold analyst says profits from a leading stablecoin operation are being funneled into physical gold at a scale that could materially impact supply and demand. After a recent meeting with insiders, he began outlining what this trend could mean for gold prices and a small group of companies positioned to benefit.

These reductions were expected given the likely loss of the SCAR business, but the market reaction feels excessive.

The six analyst revisions initially tracked by MarketBeat established a new low price target, yet still imply upside. More importantly, the average of the revised targets implies roughly 30% upside, with greater gains possible at the high end of the range.

Other indicators—rising analyst coverage, a steady Moderate Buy rating, and an 86% buy-side ownership bias—point to a more constructive backdrop. If AeroVironment can regain commercial traction and expand into new markets, analysts may lift price targets later in the year, which could spark renewed bullish activity.

AeroVironment Price Action Shows Hard Bottom at $200

There is always a risk of lower prices, but for AVAV that risk appears limited. The chart price action suggests a technical floor around $200, supported by price-volume patterns and indicator divergences. The sideways action since the March 2 sell-off following the SCAR news, combined with increasing volume on dips, suggests accumulation while momentum indicators show bears losing control.

The risk remains that selling could re-intensify, but early signs point the other way. The recent earnings release triggered a pre-market selloff that reversed into buying at the open. The divergence in stochastic and the moving-average convergence-divergence (MACD) points to a market that looks coiled like a spring and is ready to bounce higher. The key questions are how far it might climb and what will drive that move.

Key resistance levels are near $225, $240, and $250, with $250 serving as an important pivot tied to a long-term uptrend that broke in early March. Clearing $250 would be a meaningful market signal; failure to do so could allow only a muted advance, possibly topping out near $280 before the stock drifts sideways until a stronger catalyst arrives. The downside risk in that scenario is a retracement to recent lows before sustainable momentum returns. In the bull case, a move above the uptrend line could lift shares further, but $280 remains a potential short-term ceiling.

Institutions Support AeroVironment Stock Market

Institutional activity will be a deciding factor, and it was bullish heading into the earnings release. MarketBeat data show institutions own more than 85% of the stock and have been net buyers for 10 consecutive quarters, with buying activity continuing in early Q1 2026. The likely outcome is continued institutional accumulation while the shares trade at long-term lows, which should be reflected in the March ownership data.

AeroVironment's fiscal Q3 results missed top- and bottom-line expectations, but the company was up against a high bar and external events played a role. Still, underlying performance was strong: revenue grew more than 140% year over year and profitability improved.

Guidance was cautious, with revenue and earnings targets below analysts' prior expectations, though underlying metrics remain solid. The company projects growth only slightly below the roughly 135% analysts had been expecting, and its profit range brackets consensus, suggesting management is taking a conservative posture.

Potential catalysts for AVAV include continued integration of BlueHalo, sustained demand for drone platforms, execution on backlog, and the company's ability to scale production. Management is also working to diversify into commercial markets—targeting inspection, precision agriculture, surveillance, and tracking—which could add meaningful incremental revenue over time.

to bring you the latest market-moving news.

This email content is a sponsored message provided by T3 Live, a third-party advertiser of TickerReport and MarketBeat.

Contact Us | Unsubscribe

© 2006-2026 MarketBeat Media, LLC dba TickerReport.

345 N Reid Pl., Suite 620, Sioux Falls, SD 57103-7078. United States..

0 Response to "War-time stocks I bought in February"

Post a Comment