Dear reader,

Most investors run from volatility. The method I have used for the last decade turns it into a weekly paychecks.

Instead of betting on which way the market moves, this strategy harvests income from the swings themselves.

One setup. Once a week. Designed to pay, week after week — without guessing direction or day trading.

[See how volatility becomes cash flow →]

Oracle Speaks! The Message: AI Demand Outpaces Capacity

Written by Thomas Hughes. Originally Published: 3/11/2026.

Key Points

- Oracle's Q3 release affirms its robust outlook and upped the ante with improved long-term guidance, and the analysts liked it.

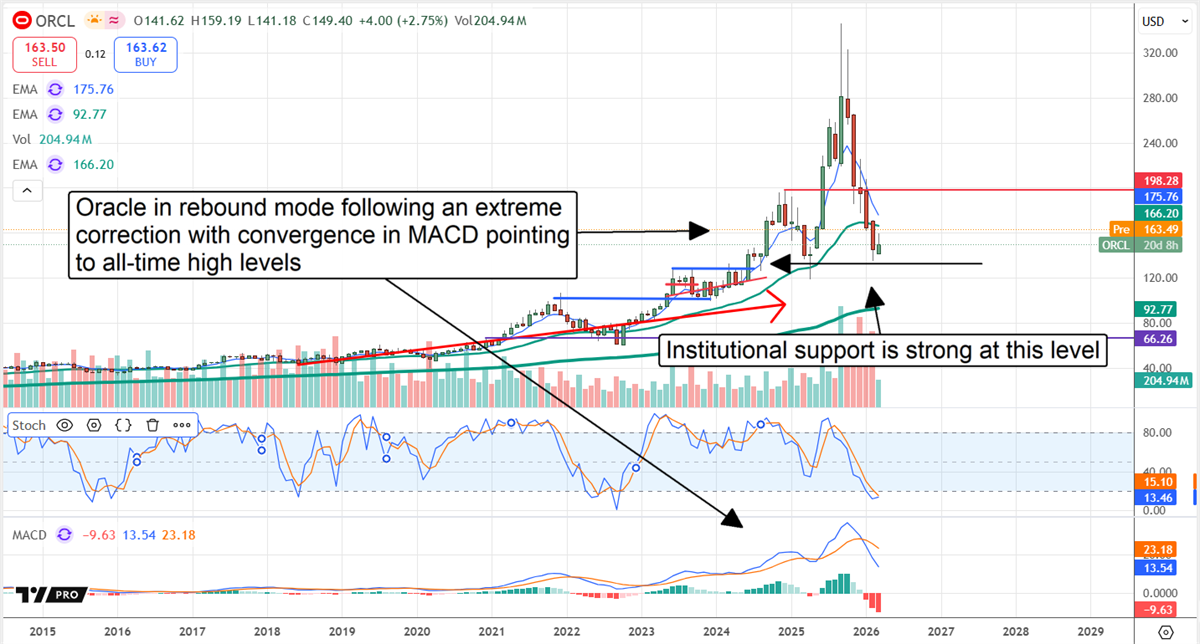

- Price target increases and upgrades point to rising share prices and the potential for a robust rebound and fresh all-time highs.

- Institutions accumulated in Q1 when prices were low, providing a support base and limiting risk in 2026.

- Special Report: The Biggest IPO Ever: Claim Your Stake Today

Oracle's (NYSE: ORCL) stock may be poised for the hottest upswing in modern tech history. The company's fiscal Q3 2026 release not only affirmed a robust outlook and eased debt-related concerns, it also raised forward guidance.

The takeaway for investors is clear: in the words of JPMorgan (NYSE: JPM) analysts, who upgraded the stock, the results provide the best evidence yet that Oracle's AI strategy is working. The company is emerging as a powerhouse of AI innovation, providing the infrastructure, development tools and AI-derived applications while improving services for both legacy and new clients.

Analysts, Institutional Buying, and Price Action Align: Robust Rebound Brewing

Iran just changed everything for gold (Ad)

The Iran War didn't just make headlines.

It broke the gold market wide open.

Gold is already above $5,000 and surging.

But the metal isn't where the real money gets made.

Go here for the full gold briefing — including the stock name and buy-up-to price >>>Analysts are responding as expected — reaffirming bullish outlooks, issuing upgrades, or raising price targets. Sentiment has shifted back to an aggressively bullish posture, reversing prior price-target reductions, strengthening the Strong Buy consensus, and improving the rebound outlook.

As it stands, the bias is firmly bullish: about 75% of ratings are Buy or stronger, the lone Sell rating is more than a year old, and the consensus price target implies roughly an 80% upside from the pre-release close. Trends are pointing to the high end of the range — the high-end target of $400 implies more than 165% upside and could be reached well before year-end.

Institutional trends also support a bottom in price action and an outlook for sustained upward momentum. While institutions sold on balance in Q4 2025, that bearish behavior ended at the turn of the new year as they returned to accumulation.

In early Q1, institutions bought about $1.50 for every $1 they sold, providing a tailwind for this market that is likely to strengthen as the year progresses.

The charts are also set up for a bullish momentum swing. Daily, weekly and monthly indicators show the stock had been deeply oversold. The likely outcome is a retest of the all-time high, with the potential to exceed it by roughly $140 — about a 100% gain. The $140 target is a base case derived from the magnitude of Oracle's recent pullback; a break to new highs would signal trend continuation and could produce gains in that range.

Oracle Rebounds on Outperformance and Acceleration

Oracle delivered its strongest quarter in more than 15 years in Q3. Revenue rose more than 21% to $17.19 billion, accelerating both sequentially and year over year and outpacing consensus by 165 basis points. Strength was broad-based, led by a 44% increase in total cloud revenue. Total cloud reached nearly $9 billion, representing about 52% of overall revenue. Cloud infrastructure grew 84%, supported by a 531% increase in Multi-Cloud Database and a 243% gain in AI infrastructure. SaaS revenue increased 13%, driven by Fusion and NetSuite.

Margins were strong as well. Oracle leveraged its revenue strength to beat consensus earnings estimates across the board despite higher spending and increased leverage. Adjusted EPS of $1.70 outpaced consensus by 590 basis points, generating significant cash flow, and management expects this strength to continue.

Guidance should propel the stock higher now that the rebound is underway. The company issued robust Q4 guidance implying better-than-forecast full-year results and raised its outlook for the following year. Oracle now expects revenue growth to accelerate to more than 31% annually, well ahead of current estimates for revenue and earnings. Drivers include rapid expansion of cloud and AI capacity, with at least another 14% to 25% increase in hyperscaler instances expected to come online in the near term.

Oracle's Debt: Not So Much a Concern as a Need

Oracle's debt and share count are increasing to support its expanding AI network. While concerns about leverage are valid, they are offset by the financing needs required to scale. The Q3 results and a swelling backlog — now about $553 million, up 325% year over year — suggest rapid expansion is necessary to capture market opportunity.

Critically, the backlog remains more than 4.4 times the company's debt, equivalent to roughly eight years of business at the Q3 recognition pace, and much of that revenue should be recognized sooner. That dynamic should enable meaningful debt reduction and growth in shareholders' equity over time. Risks include the need for additional capital, but those risks are mitigated if backlog expansion continues.

A Quiet Navy Shipbuilding Move Just Put Palantir's Software Deeper Into the Yard

Authored by Chris Markoch. Posted: 3/20/2026.

Key Points

- Keel Holdings has joined Palantir in the U.S. Navy’s ShipOS initiative, a program aimed at modernizing the Maritime Industrial Base with AI and integrated data workflows.

- ShipOS appears aligned with the federal push to rebuild U.S. maritime capacity, even if it sits outside the formal Maritime Action Plan framework.

- Palantir’s government exposure remains a central debate, but the operational work described for ShipOS also resembles problems commercial manufacturers face at scale.

- Special Report: The Biggest IPO Ever: Claim Your Stake Today

In a week when defense and aerospace stocks are competing for investors' attention, one development has flown under the radar—but it could have meaningful implications for the U.S. Navy and for Palantir Technologies Inc. (NASDAQ: PLTR).

The development: Keel Holdings and Palantir are partnering to support the U.S. Navy's Shipbuilding Operating System (ShipOS) initiative.

Iran just changed everything for gold (Ad)

The Iran War didn't just make headlines.

It broke the gold market wide open.

Gold is already above $5,000 and surging.

But the metal isn't where the real money gets made.

Go here for the full gold briefing — including the stock name and buy-up-to price >>>The program is designed to transform America's Maritime Industrial Base (MIB) through advanced artificial intelligence and tighter data integration across shipbuilders, shipyards and suppliers. ShipOS is backed by up to $4,448 million in authorized funding.

Palantir CEO Alex Karp said the partnership aligns directly with the company's mission to support U.S. military advantage.

ShipOS was first announced in December 2025, and the current news is the addition of Keel to the existing arrangement with Palantir.

"By leveraging Palantir's AI-powered ShipOS, we are taking meaningful steps to accelerate our schedules, streamline operations and enhance collaboration across the supply chain," said Keel CEO Brian Carter.

When ShipOS kicked off, 79th Secretary of the Navy John C. Phelan described the initiative as more than a software rollout—saying it "puts Palantir's cutting-edge tools in the hands of decision makers at every level" by providing real-time visibility across the supply chain.

A Proof of Concept Running Parallel to a Bigger Policy Push

Recently, President Trump signed an executive order calling for the rebuilding of the U.S. Navy's fleet.

The centerpiece of the effort is America's Maritime Action Plan (MAP), which will be supported by billions of dollars in federal funding.

While ShipOS isn't formally part of MAP, both programs fall under the Navy's Maritime Industrial Base workstream, which MAP treats as central to its revitalization approach. ShipOS appears complementary to several MAP objectives, including:

- Addressing the decline in domestic shipbuilding capacity

- Modernizing shipyards through digital tools and integrated data systems

- Demonstrating meaningful efficiency gains in production planning and execution

In short, think of ShipOS as an operational, AI-driven proof of concept running alongside MAP's broader policy and funding framework. MAP sets national strategy; ShipOS is already executing a key piece of it on the ground.

What the Skeptics May Be Missing

Palantir skeptics will note this is a government deal, and for them that underscores a perceived Achilles' heel: Palantir's reliance on U.S. government contracts.

Consider that concern in two ways. First, even if it's "only" a government contract, it's a sizable one. Valued at $448 million, it would represent over a quarter of Palantir's 2025 government revenue of $1.855 billion, which supports the view that meaningful growth remains available for Palantir.

Second, the work Palantir will perform—integrating operational data, reducing bottlenecks, compressing planning cycles and improving supplier coordination—has direct commercial applications. Three years ago the commercial side of Palantir's business was virtually nonexistent; as of the company's last earnings report, it accounts for nearly 45% of Palantir's revenue.

Palantir has moved beyond its early reputation as a black box used only for military surveillance.

PLTR Technical Setup: Key Levels to Watch

PLTR stock is up more than 15% in the last month.

Not surprisingly, investors have rotated back into the stock after the United States and Israel began military action against Iran.

That said, price action has consolidated over the past two weeks, reflecting broader market uncertainty and ongoing debate over Palantir's valuation.

Over the long haul, the bull case for Palantir remains intact.

The analyst consensus price target is around $195—roughly 2% higher than before the most recent rally. UBS recently reiterated its Buy rating and lifted its target to $200 from $180, and Dan Ives of Wedbush maintained his Outperform rating with a $230 target.

In the short term, the 50-day simple moving average (SMA) may be pivotal. Despite recent volatility, the stock has stayed close to that level. A convincing, sustained move above the 50-day SMA will likely be required for the next leg higher to begin.

to bring you the latest market-moving news.

This email content is a sponsored email for Traders Edge Network, a third-party advertiser of TickerReport and MarketBeat.

Contact Us | Unsubscribe

© 2006-2026 MarketBeat Media, LLC dba TickerReport.

345 N Reid Place, Suite 620, Sioux Falls, S.D. 57103. United States..

0 Response to "Why Fridays Can Be Paydays (If You Know This Move)"

Post a Comment