I've been tracking a financial revolution that most people don't even know exists yet.

It lets you generate $306 to $5,000 per month in retirement income…

With 10X less money than what financial advisors say you need!

This is a new type of investment you can buy with one click in your brokerage account.

Tim Plaehn

Lead Income Investor, Investors Alley

Rubrik's Selloff Could Be Cybersecurity's Hidden Opportunity

Reported by Leo Miller. Publication Date: 3/17/2026.

Key Points

- Cybersecurity stock Rubrik is down big in 2026, similar to names across the software industry.

- The company's latest earnings were much better than expected, and it looks poised to turn a profitability corner in 2026.

- While AI disruption fears fill the market, Rubrik's importance to its clients fortifies its position.

- Special Report: Elon Musk: This Could Turn $100 into $100,000

Rubrik (NYSE: RBRK) is a different kind of cybersecurity company, generating impressive growth as customers recognize the value of its differentiated approach. Most cybersecurity firms focus on preventing threats by building firewalls and managing access to information.

Rubrik takes a different tack. Rather than concentrating solely on prevention, its solutions provide value after attacks occur. Its Preemptive Recovery Engine builds a deep understanding of a client's data over time so that, after an incident, customers can recover data and resume operations as quickly as possible. The goal is to move recovery time from weeks to days, minimizing the revenue and reputational damage a cyberattack can cause.

Elon Musk already made me a "wealthy man" (Ad)

I Met Elon Musk "Face-to-Face"

During a private gathering of Wall Street elites, I was one of two people selected to speak with Elon personally.

As a result, my research now leads me to believe Elon will announce the SpaceX IPO on this date:

March 26, 2026. Circle it on your calendar.

I'm sharing an "access code" that lets anyone grab a pre-IPO stake before it happens. This is your invitation to the biggest wealth-building event of the decade.

Click Here to See how to Get Your "SpaceX Access Code"In effect, Rubrik's offerings function like cybersecurity insurance: you hope never to use them, but you'll be glad they're there if something goes wrong.

In its latest earnings report, Rubrik delivered another strong quarter. Yet the tech stock is down more than 30% in 2026, creating a potential opportunity for investors interested in a unique cybersecurity name.

RBRK Smashes Forecasts on Sales and EPS

In Q4 fiscal year 2026 (FY2026), Rubrik posted revenue of $378 million, a 46% increase. (Note: the company's fiscal reporting period is several quarters ahead of the calendar period.) The top-line growth comfortably exceeded expectations of roughly 33%.

Adjusted earnings per share (EPS) came in at 4 cents, a sharp improvement from the 18-cent loss recorded in the same period last year. Analysts had expected an 11-cent loss, so the swing into positive territory was a meaningful surprise. For the full year, adjusted loss per share was 1 cent.

The company remains unprofitable on an unadjusted basis, but its quarterly GAAP loss per share improved from 61 cents to 43 cents. For the full year, the GAAP loss narrowed substantially from $7.48 to $1.78.

Looking into the new fiscal year, Rubrik expects growth of 21% to 22%, compared with 46% in FY2026. It also expects to be adjusted-profitable for the full year for the first time, forecasting adjusted EPS between 7 cents and 27 cents. Both guidance figures topped consensus expectations.

Rubrik Pushes Back Hard on AI Disruption Risk

One of the main reasons for RBRK's sharp decline in 2026 mirrors a broader concern across the software industry: potential disruption from artificial intelligence (AI). An analyst asked whether data recovery and resilience could be "meaningfully automated by AI over time," potentially threatening Rubrik's core business.

CEO Bipul Sinha said, "I don't believe that we have any disruption risk at all from AI." That is a bold assertion, but there are several compelling reasons Rubrik may be relatively insulated from AI-driven disruption.

First, Rubrik often serves as the "system of record of last resort around data and identity." When other defenses fail, Rubrik is the system clients rely on to restore order — a role that protects customers from significant revenue loss and reputational harm.

Clients could attempt to build their own recovery capabilities or trust an emerging AI provider, but doing so carries material risk if implemented incorrectly. Given what's at stake, cutting corners on the "cybersecurity insurance" Rubrik provides could be costly.

Importantly, Rubrik's revenue is tied to the amount of data customers want to protect rather than the number of employees using the software. Unlike "seat-based" pricing, Rubrik's model won't necessarily shrink if clients replace employees with AI. In fact, broader AI deployments often increase data usage, which could make Rubrik's platform more essential. Still, the notion that Rubrik faces zero AI risk is likely too absolute.

RBRK Could Be Set Up for a Meaningful Recovery After Recent Weakness

Rubrik offers a mission-critical product, is growing quickly, and is making progress toward profitability. One notable item is stock-based compensation, which was $329 million in FY2026. That figure affects reported free cash flow — FY2026 free cash flow of $238 million is partly driven by how stock-based pay is accounted for versus cash compensation. Encouragingly, stock-based compensation fell sharply from $913 million in FY2025, and free cash flow rose more than tenfold from $21.6 million the prior year.

The MarketBeat consensus price target for Rubrik is near $91.50, implying more than 70% upside. Analyst targets updated after the company's earnings release average about $86, which would imply roughly 60% upside.

Overall, Rubrik's business appears well positioned, and its stock looks reasonably attractive following a significant sell-off in 2026.

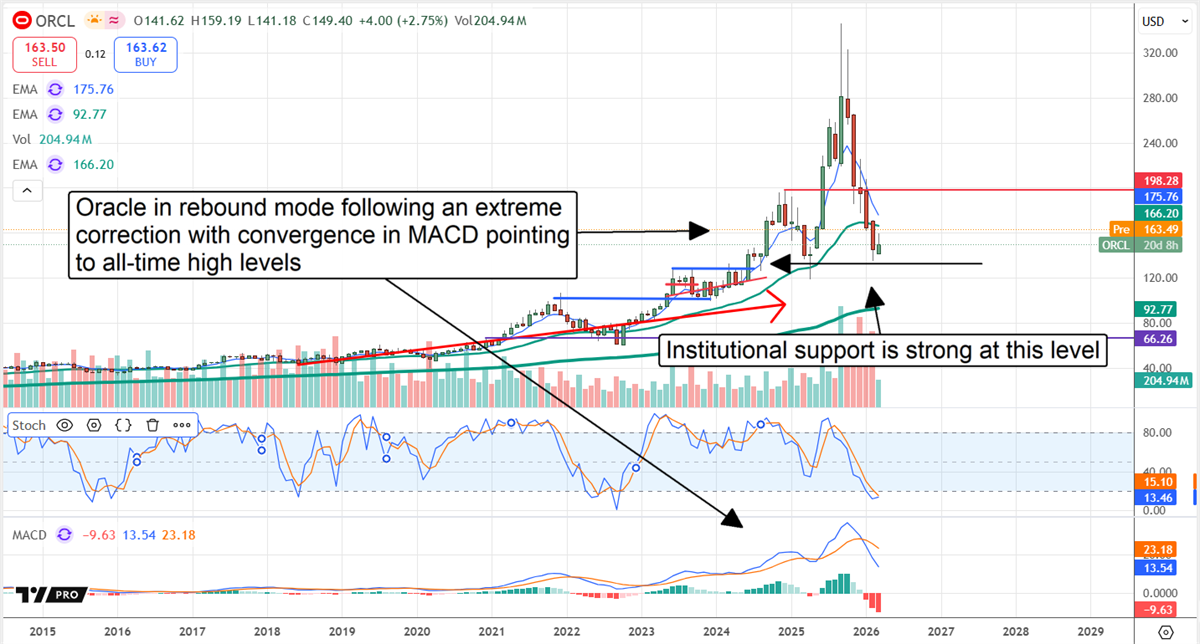

Oracle Speaks! The Message: AI Demand Outpaces Capacity

Written by Thomas Hughes. Originally Published: 3/11/2026.

Key Points

- Oracle's Q3 release affirms its robust outlook and upped the ante with improved long-term guidance, and the analysts liked it.

- Price target increases and upgrades point to rising share prices and the potential for a robust rebound and fresh all-time highs.

- Institutions accumulated in Q1 when prices were low, providing a support base and limiting risk in 2026.

- Special Report: Elon Musk: This Could Turn $100 into $100,000

Oracle’s (NYSE: ORCL) stock price could be poised to experience the hottest upswing in modern tech history. The company’s fiscal Q3 2026 release not only affirmed the robust outlook and allayed debt-related fears, but also raised the bar by improving forward guidance.

As JPMorgan analysts (who upgraded the stock) put it, the news is the clearest proof yet that the company’s AI strategy is working. Oracle is emerging as a powerhouse of AI innovation, providing the infrastructure to support AI, the tools to develop it, and the applications that derive from it — all while delivering improving services to legacy and new clients.

Analysts, Institutional Buying, and Price Action Align: Robust Rebound Brewing

Elon Musk already made me a "wealthy man" (Ad)

I Met Elon Musk "Face-to-Face"

During a private gathering of Wall Street elites, I was one of two people selected to speak with Elon personally.

As a result, my research now leads me to believe Elon will announce the SpaceX IPO on this date:

March 26, 2026. Circle it on your calendar.

I'm sharing an "access code" that lets anyone grab a pre-IPO stake before it happens. This is your invitation to the biggest wealth-building event of the decade.

Click Here to See how to Get Your "SpaceX Access Code"Analysts are responding as expected — reaffirming bullish outlooks, issuing upgrades, or raising price targets. Sentiment has shifted back to an aggressively bullish posture, reversing the trend of price-target cuts, strengthening the Strong Buy consensus, and improving the rebound outlook.

As it stands, the bias is firmly bullish: 75% of ratings are Buy or stronger, the single Sell rating is more than a year old, and the consensus price target implies roughly an 80% upside from the pre-release close, with trends pointing toward the high end of the range. The high end is pegged at $400 — more than 165% upside — and may be reached well before year end.

Institutional trends align with a bottom in price action and an outlook for sustained upward momentum in the stock. While institutions sold on balance in Q4 2025, that bearish behavior ended with the turn of the year as they returned to accumulation.

Early Q1 activity shows more than $1.50 bought for every $1 sold, providing a tailwind likely to strengthen as the year progresses.

The charts are set up for a bullish momentum swing, with indications on the daily, weekly, and monthly price charts that the market had been deeply oversold. The likely outcome is a retest of the all-time high, with the potential to exceed it by about $140 — roughly a 100% gain. The $140 figure is a base-case scenario derived from the magnitude of Oracle’s recent pullback; a break to new highs could trigger a continuation comparable to the prior move, either in dollar terms (~$140) or percentage terms (~100%).

Oracle Rebounds on Outperformance and Acceleration

Oracle delivered its strongest quarter in over 15 years in Q3. Revenue grew more than 21% to $17.19 billion, accelerating both sequentially and year over year (YOY), and outpacing consensus by 165 basis points. Strength came across the business, led by a 44% increase in total cloud revenue. Total cloud rose 44% to nearly $9 billion, accounting for roughly 52% of revenue. Cloud infrastructure grew 84%, supported by a 531% increase in Multi-Cloud Database and a 243% gain in AI infrastructure. SaaS grew 13%, driven by Fusion and NetSuite gains.

Margins were also strong. The company leveraged revenue strength to beat consensus earnings estimates across the board despite increased spending and a higher debt load. Adjusted earnings per share of $1.70 topped consensus by a wide margin (about 590 basis points), generated significant cash flow, and management expects the momentum to continue.

Guidance should propel the stock higher now that the rebound is underway. Oracle issued strong guidance for Q4, implying better-than-forecast full-year results, and raised its outlook for the following year. The company now expects revenue growth to accelerate to more than 31% annually, outpacing estimates for both revenue and earnings by wide margins. Key drivers include rapid expansion of cloud and AI capacity, with at least another 14% to 25% of hyperscaler instances coming online in the near term.

Oracle’s Debt: Not So Much a Concern as a Necessity

Oracle’s debt and share count have increased to finance an expanding AI network. While concerns about debt are valid, they are largely offset by the necessity of financing this growth. The Q3 results and a swelling backlog — now $553 million, up 325% YOY — suggest rapid expansion is required; otherwise a competitor will move first.

Crucially, the backlog remains more than 4.4 times the debt — roughly equivalent to eight years of business at the Q3 pace — and is likely to be recognized much faster. This dynamic should enable rapid debt reduction and rising shareholder equity in the coming years. Risks include the potential need for additional capital, but those risks would be mitigated if the backlog continues to grow.

to bring you the latest market-moving news.

This message is a sponsored message provided by Investors Alley, a third-party advertiser of TickerReport and MarketBeat.

Contact Us | Unsubscribe

Copyright 2006-2026 MarketBeat Media, LLC dba TickerReport.

345 N Reid Place, Sixth Floor, Sioux Falls, SD 57103. United States of America..

0 Response to "Turn your "dead money" into $306+ monthly (starting this month)"

Post a Comment