$100 Trillion "AI Metal" Found in American Ghost Town (From Brownstone Research)

AMD’s Results Sparked a Sell-Off—But That’s Your Buy Signal

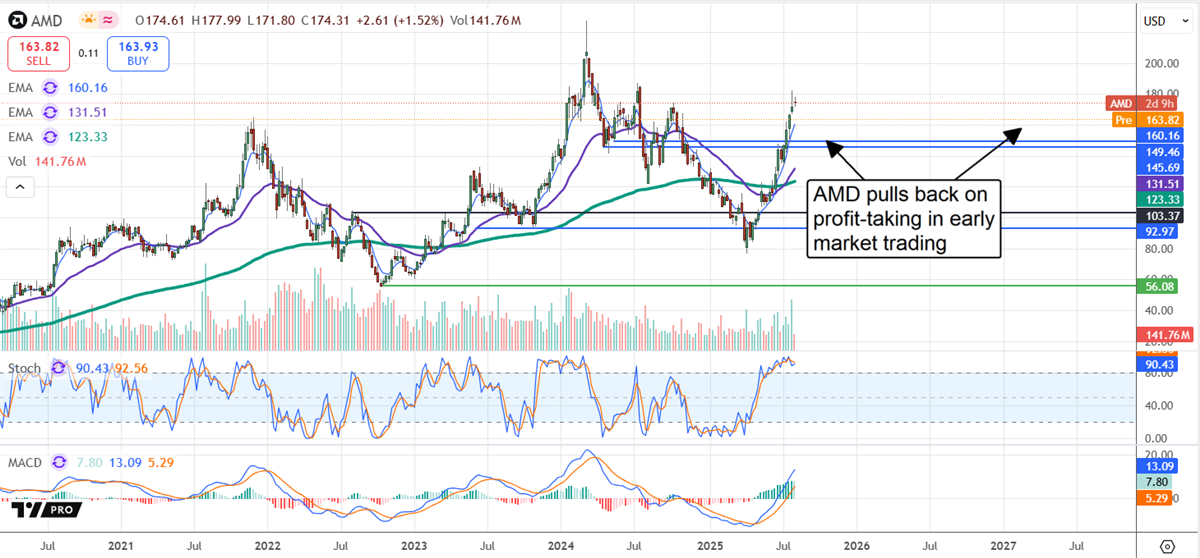

Key Points - Advanced Micro Devices gave traders a reason to take profits, but the sell-off is a time for investors to buy.

- Weak margin in Q2 is due to restrictions on China: recovery is forecasted in Q3 with or without the resumption of sales to China.

- Analyst trends are leading this stock to a new all-time high that may be reached this year.

AMD’s (NASDAQ: AMD) Q2 results were tepid, giving the market a reason to sell, at least for some participants. The results and subsequent sell-off also provide a reason to buy, having missed a high bar by a slim margin due to misplaced expectations and providing a discount to recently elevated prices. The primary cause of Q2 weakness and the sell-off is the decline in margins and earnings. As expected, restrictions on semiconductor sales to China impacted the margin. The Trump administration has since reversed the restriction, but the license to sell has yet to be granted, which isn’t all that surprising. Until then, business outside China has remained strong, and the outlook is robust. The Trump economy is back in full force, and it's creating huge opportunities for investors.

With Trump pushing for lower taxes, fewer regulations, tariffs on foreign competitors, and domestic manufacturing dominance, some stocks are set to skyrocket in value—while others will be left behind.

That's why we put together this free report revealing the 7 MAGA stocks poised to thrive in 2025. 🔻 Download the full report now and get the inside track on these 7 powerhouse stocks. Advanced Micro Devices Sustains Momentum: Market Share Gains Expected in 2026 Advanced Micro Devices had a solid quarter with revenue growing by 31.7% to set a record $7.69 billion. The company has doubled in the last four years and is on track to double again over the next few years as its next-gen, rack-scale solutions become commercially available and market share is taken from NVIDIA (NASDAQ: NVDA). Revenue is also better than expected, driven by strengths in all segments, revealing the strength of the company’s position. The AI, data center, and GPU segments are strong, and server and PC-related sales also set records. Segmentally, the datacenter grew by 14%, client and gaming by 69%, and the embedded segment contracted by 4%. The margin news is a sticking point for investors in Q3, with the GAAP and adjusted margin contracting sharply compared to last year. However, the contractions are primarily non-cash, related to China–focused inventory, and are not expected to continue in future quarters. The guidance for Q3 is not only stronger than expected, with revenue forecast to grow by another 28% year over year, but the adjusted gross margin is expected to rebound to normalized levels, and it does not include sales in China. “Our current outlook does not include any revenue from AMD Instinct MI308 shipments to China as our license applications are currently under review by the U.S. Government.” Undervalued Advanced Micro Devices Builds Equity Cash flow and free cash flow are important factors for investors to consider. The company’s free cash flow also reached a record level, enabling it to maintain a healthy balance sheet, continue investing in its future, and create value for shareholders. Quarter-end highlights include increases in cash, investments, and inventory, as well as current and total assets, with total assets rising by 8% or $5.6 billion. The critical details are that asset gains outpace liability increases, leverage remains ultra-low with long-term debt less than 0.1x the equity, and equity is up by 3.7% including an increase in treasury shares. The company doesn’t repurchase shares aggressively but offsets share-based compensation and keeps the count relatively flat yearly. Regarding valuation, this company trades at a relatively high 45x the current year estimate but only 14x the 2030 outlook, which is a deep value price point. Based on the current year outlook, leading tech blue chips tend to trade in the 25x to 35x range, suggesting this stock could double to triple in value over the next five years. Profit-Taking Opens Opportunity: Robust Rebound Is Expected AMD’s post-release price plunge is profit-taking as much as anything else. The market for AMD stock rose by more than 100% from April to early August, providing plenty of profits for savvy traders. However, the technicals remain bullish, and the outlook is favorable, with the market above critical support levels and likely to rebound quickly. The critical support level is near $150, but strong support may be present at a higher level. The initial analyst response is bullish, aligning with the trend and technical outlook. The first revision picked up by MarketBeat is an increased price target from TD Cowen to an above-consensus $195; the chatter centers on upcoming sales and the launch of MI400 products. The increase puts the market in the high-end range, which tops out at $270 in early August, a 50% price increase from the critical support target and a new all-time high when reached.

Written by Thomas Hughes Read this article online › Read More:

Did you learn something from this article?

|

0 Response to "AMD Sell-Off: Your Prime Buying Opportunity"

Post a Comment